Business Transitions – Workshop 1 (Business Evaluation)

The Appleton Greene Corporate Training Program (CTP) for Business Transitions is provided by Mr.Sussman MBA BS Certified Learning Provider (CLP). Program Specifications: Monthly cost USD$2,500.00; Monthly Workshops 6 hours; Monthly Support 4 hours; Program Duration 18 months; Program orders subject to ongoing availability.

If you would like to view the Client Information Hub (CIH) for this program, please Click Here

Learning Provider Profile

Mr Sussman is a Certified Learning Provider (CLP) at Appleton Greene and he has experience in management, operations and finance. He has achieved an MBA and a BS in Management. He has industry experience within the following sectors: Technology; Telecommunications; Internet; Business Services and Real Estate. He has had commercial experience within the following countries: United States of America, or more specifically within the following cities: Dallas TX; Chicago IL; Los Angeles CA; New York NY and Indianapolis IN. His personal achievements include: founded, financed, grew, profitably operated, built value and transitioned five businesses via sale transactions, 3 of them to public companies and 2 to strategic acquirors; served as a C-Suite executive at two public companies; one time as President of an operating division and the other as Vice President of Mergers and Acquisitions; raised over $500M in private equity and both private and public debt offerings for clients; built value for 100s of businesses by Improving their sales, profitability and operational performance; holds and maintains FINRA Investment Banking Licenses for both public and private placements. His service skills incorporate: capital investment; process Improvement; mergers & acquisitions; business development and strategic planning.

MOST Analysis

Mission Statement

Course Objectives:

Business Transitions is a forward-looking program designed to build value for the next evolution of the business. Business Transitions begins with establishment of a baseline for where the business is today. Business Transitions are affected by the value of the business viewed by industry standards and balanced against the perceptions, desires and needs of the owners and stakeholders of the Company itself. To accomplish this, a suite of tools will be utilized. In this session, we will be introduced to, and learn each tool for use and application throughout the Business Transitions program. These tools are; Porter’s Five Forces, SWOT, 5 Whys: Root Cause Analysis, VMOST Analysis and Pareto Principle. Each of these tools will facilitate analysis into each area and identify areas and create a roadmap for improvement and change to build value.

Objectives

01. The changing business environment today: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

02. Understanding the impact of external economic activity on business growth and success; departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

03. How to set objectives for your business; departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

04. Metrics for measuring business success; departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

05. Evaluating business performance in the modern economy; departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

06. Porter’s five forces; departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

07. SWOT analysis: departmental SWOT analysis; strategy research & development. 1 Month

08. Root cause analysis: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

09. VMOST analysis: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

10. Pareto principle: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

11. Appraising future investments: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

12. Implementing improvements and growth measures: departmental SWOT analysis; strategy research & development. Time Allocated: 1 Month

Strategies

01. The changing business environment today: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

02. Understanding the impact of external economic activity on business growth and success: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

03. How to set objectives for your business: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

04. Metrics for measuring business success; Each individual department head to undertake departmental SWOT analysis; strategy research & development.

05. Evaluating business performance in the modern economy: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

06. Porter’s five forces: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

07. SWOT analysis: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

08. Root cause analysis: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

09. VMOST analysis: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

10. Pareto principle: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

11. Appraising future investments: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

12. Implementing improvements and growth measures: Each individual department head to undertake departmental SWOT analysis; strategy research & development.

Tasks

01. Create a task on your calendar, to be completed within the next month, to analyze The changing business environment today.

02. Create a task on your calendar, to be completed within the next month, to analyze Understanding the impact of external economic activity on business growth and success.

03. Create a task on your calendar, to be completed within the next month, to analyze How to set objectives for your business.

04. Create a task on your calendar, to be completed within the next month, to analyze Metrics for measuring business success.

05. Create a task on your calendar, to be completed within the next month, to analyze Evaluating business performance in the modern economy.

06. Create a task on your calendar, to be completed within the next month, to analyze Porter’s five forces.

07. Create a task on your calendar, to be completed within the next month, to analyze SWOT analysis.

08. Create a task on your calendar, to be completed within the next month, to analyze Root cause analysis.

09. Create a task on your calendar, to be completed within the next month, to analyze VMOST analysis.

10. Create a task on your calendar, to be completed within the next month, to analyze Pareto principle.

11. Create a task on your calendar, to be completed within the next month, to analyze Appraising future investments.

12. Create a task on your calendar, to be completed within the next month, to analyze Implementing improvements and growth measures.

Introduction

Introduction to Business Evaluation Course

Success in the changing business environment of today is only available by identifying the importance of updates and innovative measures. Before we discuss the important subject of business evaluation, it is necessary to shed some light on the changing business environment that has resulted in the need for businesses to constantly evaluate their strategy and growth curve.

Changing with time is a key business skill and as an introduction to our business evaluation course we will look at some necessary techniques for adjusting in the rapidly changing business environment of today.

Steps for Change Management

The changing business environment has only made senior executives realize the needs of their employees. When change was scarce, organizations wouldn’t worry about ingraining it within their culture and employees, but now that change lies at the very core of business culture, there is greater focus on how it can be managed and the results that can be derived through it.

Some steps organizations and managers can follow today to remain competitive in the changing business environment include:

Addressing the Human Side

Almost any significant transformation in the workplace can create people-issues and complications. New skills and capabilities have to be developed, new leaders will be asked to step up and fill in for responsibilities. Employees will remain skeptical of change in the meanwhile and will have their reservations as always.

Dealing with these issues in a reactive manner can put all morale, efficiency and speed at risk. The first and perhaps the most important attribute of change management should be to focus on the employees directly involved in the process. The change management process can only succeed if the focus remains on employees and what that change means to them. The change management approach should be integrated into the decision making process and should focus on employees as the first point of change.

Starting from the Top

Since change can be inherently unnerving and unsettling for people at all levels of an organization, the attention would definitely turn to the leadership team and CEO for support, strength and direction. Leaders themselves have to be onboard with the new approaches first and should be ready to take drastic measures for the growth of the organization. These drastic measures should be focused on challenging and motivating the organization. Executive teams should be the first to be introduced to the change and should be kept on board throughout the change.

Involving Every Layer in the Firm

As transformation programs progress forward, you should look to involve every layer within the organization. Change efforts should include plans to identify leaders across the organization and give them dedicated instructions on how to manage a change initiative. Since water trickles down, the implementation of the change initiative should start from the top and then trickle down to the bottom. The change eventually cascades through the organization and achieves the objectives required from it.

Creating Ownership within Workers

Leaders of real change management programs strive to create ownership among the workforce in favor of the change and what it can achieve for the organization. This can be created through a leadership team willing to accept responsibility for the change in all areas they can influence or control. Ownership can be created and reinforced through the use of rewards or incentives. The incentives can either be tangible, in the form of financial compensation, or intangible, in the form of psychological camaraderie and a shared sense of destiny.

Assessing Culture

Almost all successful change management programs pick up intensity and speed as they come down to other lower levels of the hierarchy. This is only possible if the management has done their homework and assessed all attributes of the organization’s culture. Companies often assess culture too late and do not recognize the importance it carries. Through cultural diagnostics, organizations can prepare themselves for change, bring a number of major problems to the surface, define all factors that influence leadership sources and identify conflicts. These diagnostics help in the identification of core values, behaviors and perceptions across all levels of the organization.

Adapting to Change in a Changing Business Environment

As managers and employees in this changing era, the primary measures you can take to adapt to and be ready for change include:

• Becoming aware of your situation

• Understanding the true meaning of change and how it inspires you

• Building your skill- and knowledge set for the future

We explore these points in greater detail within this section.

Becoming Aware of Your Current Situation

A big part of change management for supervisors and managers is to become aware of their current situation. What is currently going on in your organization? If you don’t know, it is about time that you find out about it and take the steps necessary to inculcate change within the workplace.

Relevant ideas and questions to help you take the research process and pace forward include:

• What is the mission of your specific department, organization or unit? Supervisors and managers need to begin their analysis of the current situation by answering this question first. The very first thing to clarify is your department’s or unit’s mission. Concrete steps toward change can only be undertaken once the mission is clear.

• What is the purpose of your job? As supervisors and managers, we contribute to the organization in one way or another. The job has a specific purpose, which should be identified and understood here.

• What are your key assignments and responsibilities? Again, supervisors should take their understanding of the job’s purpose forward by studying the key responsibilities and assignments that come under their supervision. An understanding of these responsibilities can significantly enhance results.

• What does your supervisor expect from you? As employees, and even as managers, we mostly have supervisors and higher-ups keeping an eye on us. These supervisors expect a certain deal from all members.

• What obstacles stand in the way of change? Organizations and the employees within them should identify all obstacles in the way and come up with a clear strategy to remove these hurdles and build a clear path to success.

• What resources are present at your disposal? The basic economic problem of limited resources and unlimited wants still stands true today and should be mitigated before proper change management. Understand the resources you have and take the query of wants forward from there.

• What changes are coming? Finally, you should ask yourself the all-important question of what changes are coming your way? This answer helps you determine the management endeavor and adapt to change along with your team.

The inability to answer questions like these should be a warning for most department managers to do their homework. As managers and supervisors, you are in a very strategic position in the change management process. The inability to do your homework can significantly reduce the efficiency of change.

People in organizations often employ selective perception, specialization or certain habits to keep them from being exposed to ideas of change. While this can be considered basic human nature, it isn’t a good strategy to handle change. Instead, this is the time for supervisors and managers to look into their fears and broaden the information they have to explore a number of new ideas. By increasing their awareness of change, managers can practice a distinct advantage over others who have isolated themselves.

Understanding Change

Compare your reaction toward change to that of a small child’s reaction to thunder. You might ignore change as it comes your way, but a small child may feel anxious and can seek assurance from the adult sitting them. It is a basic human trait to fear the unknown, as confidence only comes from understanding the phenomenon and the intricacies behind it. From your learning and experiences as an adult, you now realize that thunder is a natural event that does not harm you. The small child has no idea what thunder is and can only hear a loud, roaring sound that immediately scares them. Based on this analogy, an important step toward change is to realize and understand what is happening around you and why you’re a part of it.

Is your department in the process of being reorganized? Are you a bit worried about how that might impact you? These reactions are totally natural. But do not fall victim to speculations, inclinations or rumors that make you assume the worst. Wait for someone to explain the motive behind the reorganization, and the specific changes that will result from it.

Flexibility toward change can make organizations stand out in the industry today. Organizations that fail to deal with change are unable to compete with other strong members in the industry. Organizations can have internal debates on this matter, but as a rule of thumb, organizations should appreciate technology and competition, and also recognize that these two factors play an important role in business evaluation and re-evaluation.

Building Skills

Adapting to change frequently requires an effective command over skills that matter in the industry today. In some cases, adapting to change will require you to learn a number of new skills that you do not yet have command over. As employees and managers, we cannot stop learning and updating our skills.

Employees should take the responsibility to educate themselves and also to remain current and up to date with changing trends. This information will help update their skill sets and will also demonstrate an achievement and strive toward self-improvement.

Considerations to Stay Relevant in the Changing Business Environment

The faster you learn, the sooner you can adapt to changes and the more relevant you will remain in the industry. One of the biggest challenges that leaders face today is facilitating organizational adaptability. The business environment, as we have discussed above, is dynamically changing around us. There are a number of new advancements and challenges that weren’t around until recently and have popped up of late.

Historically, western culture has focused on the concept of a heroic leader. The idea that a charismatic leader will swoop in as the knight in shining armor and save the business in distress has for long been the ideal characteristic that businesses and entrepreneurs have had to live up to. For instance, take a look at the cover of any business magazine and you will see pictures of the successful CEO and the achievements they have had, without a single word on the team that helped them achieve what they did.

As per recent business predictions, businesses that live by the same age-old methodology and don’t broaden their leadership practices will suffer at the hands of the changing business environment of today. Change will upgrade you onto a phase of relevance, be it from customers, competitors or even suppliers.

In this section we shed light on some of the considerations and practices businesses can follow to remain relevant in this changing business environment:

Updating Change Theory

Just like the business environment around us is constantly evolving, so too are the leadership and change theories enabling work. Unfortunately, many theories of change are focused on antiquated efforts that don’t hold true anymore. For instance, the trickledown effect does hold value, but the fact that one person at the top can impact almost every aspect of an organization’s style and environment is insane. Every hierarchy in the organization comes with different approaches, environments, cultures and behaviors. Due to the difference in these core processes, the behavior toward change and the acceptance of new technologies will be different across the board. Hence, leaders cannot just impact every level within the organization by cascading goals, directions and values.

Organizations need to take into consideration the emergence of sub-cultures across hierarchies and the different dynamics across different levels. Based on this information, viewing the entire organization as a stable entity with similar characteristics and viewing the leader as the messiah in a white robe is plain farfetched.

Shift from Drastic Change to a Culture of Adaptability

The primary assumption with the change process is that it is something that begins and then ends, once it has lived its finite life. A change effort, for instance, connotes a finite effort that is temporary and will not last long. Hence, organizations and employees really aren’t at fault to consider change a temporary effort which will pass when people start suffering change fatigue.

However, change isn’t something that ends, especially in the rapidly changing business environment of today. There is no single change per se, just varying levels of organizational adaptability toward different advancements.

Organizational adaptability can be defined as an organization’s ability to do something in a sustainable manner without interruptions. However, organizational adaptability requires a shift in perspective from top management, who should focus more on short-term management than on long-term management.

Distinguish Between Managers and Leadership

Many leadership training and development programs in the contemporary world focus a lot on individual skill sets such as delegation, building a strategic vision and coaching. While these leadership skills can be helpful for managers, they aren’t a true representation of leadership.

While leader development focuses primarily on the individual and their skills, leadership development focuses more on creating value through interaction in the workforce. Organizations looking to promote true leadership development should give opportunities to all leaders to apply their skill sets within their work. This includes producing real results through collaborative inquiry, action learning and appreciative feedback. The faster leaders learn, the faster they can adapt to different situations.

Clarify the Purpose of Leadership in Your Organization

With the growing surge in cross functional teams, the role of the leader in organizations is a lot more prominent. As the business environment changes at a rapid pace, leaders have to act as liaisons and integrators that enable the coordination of disparate functions across the organization. Based on leadership theories from prominent psychologists, we can list down three major types of leadership styles:

• Administrative Leadership: This leadership style is focused on coordinating and structuring organizational activities in a bureaucratic manner.

• Adaptive Leadership: Adaptive leadership is what is seen when a meeting that starts with opposing viewpoints and different arguments ends on a positive note of consensus.

• Enabling Leadership: Enabling leadership refers to the conditions leaders set to enable new behaviors, learning and innovation.

The purpose and type of leadership should shift based on the situation organizations find themselves in, and the steps that should be taken to counter that situation.

The Effect of Economic Change on Businesses

Sometimes organizations feel like the only guarantee about economic conditions is that they will change sooner or later. Businesses with sufficient experience behind their back went through the same phenomenon yet again as COVID-19 killed all economic activity and led to a recession of sorts. These economic ups and downs are part and parcel of running a business, and business owners can’t help but be aware of them and the complications they bring for them. Due to the constant presence and threat of economic downturns, businesses have to ensure that they are always working toward plans for better economic strength and ability.

In this section we study the impact economic conditions can have on business activity:

Focus on Profitability

Regardless of how the economy is doing, the primary focus of every organization today should be on making their business as profitable as they possibly can. As a general rule of thumb, seasons of high economic growth and stability are relatively easy for businesses to manage. This is because economic growth is the call of the hour, consumer confidence is high, unemployment rates are down and people have greater disposable incomes to spend on goods they like and believe they should have. All of this eventually leads to more people choosing to buy from different businesses. The more people have to spend, the more willing they will be to try different businesses in the market and benefit from the expertise they have to offer.

This situation can present a gloomy contrast when economic activities die down and the economy experiences a downturn. People are more inclined toward saving money during an economic downturn than they are toward spending it. Additionally, businesses also have to market hard to build a relative perception of their product in the eyes of customer. Businesses can feel the pressure during economic downturns, especially if they aren’t prepared to face the rising pressure.

Business entities that are focused on being profitable get to benefit the most during dry times of economic downturns. The objective of profitability does not only provide businesses with the peace of mind they require across seasons, but it also gives them the freedom and leverage to make hasty cuts in prices during recessions, make rash decisions based in the moment and innovate their product for different markets. Without the freedom to experiment with decisions, businesses will never be able to decide what’s best for them. This will eventually lead to a sphere of decreased sales, where businesses rely on past glory and profits to pull them through the phase.

Be Prepared for Opportunity

This does sound like the kind of content you might see on the marketing material for a business school, but the fact of the matter is that every single economic period brings with it an opportunity for businesses to diversify their opportunities and open new avenues.

During a period of growth, businesses are more at ease to take decisions they feel can be beneficial for them and are also willing to hire additional personnel, because there is no better time than now. Organizations that want to move into larger spaces also do so during periods of economic downturn, because the market is ideal for purchasing during such periods, and businesses have enough cash available to them to buy new plants and step into new markets.

Lean sessions of economic downturn can present a different kind of opportunity altogether. These opportunities are difficult to jump on, as most of the businesses in your industry might decrease their operations and reduce the money they spend on marketing.

As your competitors reduce the focus they put on the market, you can focus intently on pivoting your efforts to focus more on new avenues such as digital marketing, entering a new market or crafting a new marketing strategy. These seasons also give you the time and freedom to experiment with new packages, pricing tiers and services that they haven’t embarked on previously.

The exciting part about opportunities unearthed during periods of economic downturn is that they pave the way for future growth in this regard.

External Factors Affecting Business Environment

There are a number of external factors today that impact business environment and the success/growth curve of organizations around us. While we have discussed the economy in general and the impact it has on businesses, we will discuss some of the other external factors that affect business performance and can positively or negatively influence growth.

1. Social and Cultural Environment

The social and cultural environment of a region includes the attitudes, values, opinions, lifestyles and beliefs of individuals residing in a nation or region. These characteristics determine customer behavior and are developed from cultural, demographical, religious, ethnic and educational conditioning. The characteristics are often the result of years of conditioning.

Like other forces impacting the external business environment, social factors keep changing continuously. A change in the social attitudes, values and beliefs in a region can affect the demand for different types of leisure activities, books and attire etc.

The factors that influence this impact include:

Demographic Factors

Demographic characteristics such as age distribution, population, literacy levels, religious composition, inter-state migration, income distribution and rural-urban mobility can significantly influence the strategic plans of an organization. This eventually affects the compensation and hiring policy followed by employers within different organizations.

The age demographics in particular countries define the selling and buying environment of that region. Organizations have an eye on the characteristics and the age demographics of the people in the region and make their plans accordingly. Countries with a growing young population have a shift toward more youth-oriented goods, which are meant for younger audiences. These products include fitness equipment, beauty products, magazines, hair and skin care preparations, etc.

On the contrary, countries with a growing population of senior citizens have businesses that focus more on products to this market. Additionally, governments in such countries pay more importance to social security benefits and tax exemptions for senior citizens.

Cultural Factors

Social values, customs, attitudes, rituals, practices and beliefs are formed through years of conditioning and influence businesses and their practices in a number of ways. Christmas offers a great opportunity for tree growers, toy retailers, card companies and mail order catalogue firms to grow their business further and to benefit from the sudden spike in demand.

Social values can best be defined as an abstract sense of what is good, desirable and bad. Beliefs on the contrary can be defined as an understanding of the characteristics that define social and physical phenomena around us. Beliefs are important, since they define the way most individuals think and the rules they have for themselves.

McDonald’s is the ideal example of a foreign brand endorsing local culture and beliefs to sell in different markets. Being a global brand, McDonald’s is present in a number of countries across the globe. The fast food brand does not serve beef burgers in India, because practicing Hindus within the country consider cows to be sacred and prohibit the consumption of beef. Values and beliefs vary from country to country, and organizations should always consider them before stepping into different global markets.

This concept can better be defined through the consumption of soup in both, the United States and Japan. When marketing soup in the United States, restaurant managers and marketers realize that soup works best as an appetizer and builds the appetite for what’s to come, which is why it is best marketed in that role. However, the marketing and positioning of soup would be completely different in the Japanese market. Soup is considered a breakfast drink in Japan, which is why brands market it in that way.

Religious and Ethical Actors

Religious beliefs often dictate the consumption patterns of most users across the globe. Since Muslims, the followers of Islam, are prohibited from eating pork, they don’t have bacon for breakfast or any other meal made out of pork for that matter.

Similarly, religious beliefs set the foundation for ethics as well. The culture of different countries is dictated by the primary religion within the region.

2. Political Environment

Many political factors in the environment businesses operate in can influence how managers implement strategic decisions and how they formulate ideas for the business. The political environment of a nation determines a number of factors including high tariffs, barriers to entry in a nation, anti-nationalist slogans directed toward foreign brands, bad publicity and a lot more.

While businesses do not want to be involved in modern politics, they do realize that successful growth across countries in the world requires a basic understanding of the laws of the land and how things work in the region. From tax laws to tariffs, business treaties and commerce in general, a number of factors can be influenced by the politics of the region.

These factors are:

• Political climate

• Severity of employee welfare legislation

• Influence of political pressure groups

• Political influence on trade unions

• Protection of special interest groups like consumers, women, minorities

• Simplicity and understandability of government legislation

• Consumer protection laws

• Environmental pollution control legislation

• Government’s view on globalization and trade liberalization

• Political stability

• Political ideology and philosophy of political party in ruling

• Environmental protection laws

• Anti-monopoly laws

• Export restrictions

• Copyright and patent protection

Some of the ways politics can influence businesses include:

Politics and Business Taxes

Businesses with a higher yearly yield are typically taxed at a higher percentage than businesses that earn within a lower bracket. Businesses in the modern economy need to understand the importance of paying taxes and should recognize that there is no way out of the conundrum. Taxation is an important part of business today.

Business owners also keep an eye on the exchange of rhetoric between the ruling party and opposition parties. Opposition parties are often in favor of reducing taxes on bigger organizations. The pressure put on them by the opposition can eventually determine the response of governments toward progressive taxation measures. A major increase in taxation for foreign brands can also scare a number of brands away from the local market.

Employee Protection and Coverage

Businesses expanding operations across the globe have to keep an eye on the individual employee protection and coverage requirements that are in place by ruling parties in different countries. Different countries have different regulations on minimum wage, health benefits and other instances of employee protection and coverage. A detailed look at these legal factors should clear complications away.

International Business Impact

No business can succeed within a bubble. Sure, an organization can operate on a local level and have customers from within the local region or community, but almost all company owners and investors dream for their organization to go big and have a global impact on proceedings around us. Political tensions on a global level can impact local businesses as well, since countries’ economies today are all connected in a certain way.

For instance, the departure of the United Kingdom from the European Union negatively impacted a number of local businesses, which although operated on a local scale, had to look at new ways to do business.

Business and politics have an incredible connection, which is something that we will take a look at in greater detail through the length of this manual. The business world can collide with the world of politics in a number of scenarios to create economic openings for the society at large.

3. Legal Environment

The regulatory environment or the legal framework in most countries is decided by the political party in power within the upper house. The government, hence, has the power to legislate on and discuss matters like managerial remuneration, wage fixation, location of plants, safety and health at work, price control, location of plants, licensing policy, entry of multinationals and export policy.

Most mixed economies with a certain level of control exercised by the government follow the same characteristics – the government puts down the rules of the game, while businesses in the industry are required to follow them to the letter.

Companies that want to operate on a global level should study the law of the land in detail and adapt to the requirements it puts on them. The legal framework of all international countries should be respected for the right results.

4. Technological Factors

New technology can be utilized in a number of ways to counter both, recession and inflation. New machines come with capabilities to reduce production costs and can help businesses succeed in what they do. Current advances in information technology have made it possible for global supply chain players to plan for the future and have also enabled them to distribute their products economically in better quantities than before.

Technology is the means by which a business converts all input, including raw materials, into output in the form of finished goods. By this definition, technology can refer to anything that helps in the production process including machinery, tools, work procedures, equipment and employee skills and knowledge.

In the competitive world of today, breakthroughs in the field of technology can significantly influence the efficiency of an organization itself and the stakeholders that it is associated with. Technology can impact the efficiency of the service market a business is trading in, the suppliers, distributers, customers, competitors, manufacturing processes and marketing processes.

During the last few decades, we have seen a greater focus on technology that promotes communication within and outside of organizations. Optic fibers have facilitated technology in communication, robots have completely changed the face of manufacturing processes, digitalization has enhanced the delivery of sound and image output, lasers have come up as the perfect alternative for scalpels in a number of surgical procedures and computers have helped in the processing and structuring of enormous amounts of data.

Technological advances help open up a number of new markets as well. Since technology is an ever involving concept, organizations have to keep a stringent eye on it. Failure to monitor tech trends and evolve according to the requirements can lead to your products becoming old and obsolete. Keeping an eye on technological trends and advancing with the world as it proceeds forward can help organizations flourish in a competitive market. Organizations can also create new competitive advantages through the use of tech sources.

It is technology that helped Dell implement a new inventory management system and flourish in global markets without inventory in hand. It is technology that has helped banks and financial institutes place a number of ATMs across convenient locations to make transactions easier for everyone involved.

5. International Environment

The international business environment can significantly impact the ability of a business to operate on a global level. Fluctuations of the local currency against those of the foreign country can reduce the assets of the company.

Additionally, the emergence of competitors in the international business environment can also shake the grounds that you stand on. Your local market will most definitely opt for that competitor as well, sooner or later, which is why businesses have to keep giving their best, regardless of whether they have a local competitor or not.

Once the concept of change in the business world today is understood, organizations can successful enter a strategic period of success. Business evaluation is based on identifying the changes in the market and setting objectives accordingly.

Just like you would build good individual habits while achieving and fulfilling personal goals, you should live by the same principles while achieving business objectives. The actions that achieve the KPIs of business growth can be honed through decent business practices and constant evaluation.

Executive Summary

Chapter 1: The Changing Business Environment Today

Not too long ago, senior executives in larger organizations had a simple goal set for the growth of an organization – stability. Shareholders did meddle in internal affairs, but they were ultimately concerned only with predictable earnings growth. A predictable and accurate earning potential/dividend would get shareholders off their back and give managers the peace of mind they require.

Since so many markets were underdeveloped, leaders could work on annual exercises to deliver on expectations. The strategic plan remained the same across the organization, with only a few modifications for small strategic teams. Prices remained in check, people were happy with their jobs and life was relatively good.

The recent shift toward labor mobility, market transparency, instantaneous communication, global capital flows and the ability to improve with time have blown the comfortable scenario of yesteryears to smithereens. Almost all companies today, from market giants to startups, their collective interest lies in something that was happily avoided and slightly ignored in the past: change.

Challenges of Change

The heightened focus on change presents most senior executives and managers with an unfamiliar challenge of sorts. Almost all organizations today devise their best tactical and strategic plans with an eye on change management. Change in the business environment was welcomed with jubilation, but that very change now presents challenges for businesses trying to cope.

All factors in an organization, from its values to company culture, people and behavior, need to be aligned for the right results. Plans and motives of change do not create the results intended from them. In fact, value is captured and realized through the collective and sustained actions of thousands of employees and the organization.

A long term structural transformation has 4 major characteristics:

1. Scale: The change should affect all or most of the organization as a whole.

2. Magnitude: The change should significantly alter the set status quo.

3. Duration: The change should preferably last for months, if not years.

4. Strategic Importance: The change should be important in relation to the strategic

objectives of the organization.

Many senior executives respect these characteristics, but also realize that real rewards of change can only be reaped if the change occurs at an individual level. Many CEOs and change managers are kept up at night at the thought of how people will react to change, especially since it is now a major part of the workforce. Managers also fret over what can be done to maintain the company’s unique values and original culture over this period of change. Change can have a number of positive attributes, but it can also debilitate progress and all the years of hard work if it isn’t monitored carefully.

Steps for Change Management

The changing business environment has only made senior executives realize the needs of their employees. When change was scarce, organizations wouldn’t worry about ingraining it within their culture and employees, but now that change lies at the very core of business culture, there is greater focus on how it can be managed and the results that can be derived through it.

Some steps organizations and managers can follow today to remain competitive in the changing business environment include:

Addressing the Human Side

Almost any significant transformation in the workplace can create people-issues and complications. New skills and capabilities have to be developed, new leaders will be asked to step up and fill in for responsibilities. Employees will remain skeptical of change in the meanwhile and will have their reservations as always.

Dealing with these issues in a reactive manner can put all morale, efficiency and speed at risk. The first and perhaps the most important attribute of change management should be to focus on the employees directly involved in the process. The change management process can only succeed if the focus remains on employees and what that change means to them. The change management approach should be integrated into the decision making process and should focus on employees as the first point of change.

Starting from the Top

Since change can be inherently unnerving and unsettling for people at all levels of an organization, the attention would definitely turn to the leadership team and CEO for support, strength and direction. Leaders themselves have to be onboard with the new approaches first and should be ready to take drastic measures for the growth of the organization. These drastic measures should be focused on challenging and motivating the organization. Executive teams should be the first to be introduced to the change and should be kept on board throughout the change.

Involving Every Layer in the Firm

As transformation programs progress forward, you should look to involve every layer within the organization. Change efforts should include plans to identify leaders across the organization and give them dedicated instructions on how to manage a change initiative. Since water trickles down, the implementation of the change initiative should start from the top and then trickle down to the bottom.

The change eventually cascades through the organization and achieves the objectives required from it.

Creating Ownership within Workers

Leaders of real change management programs strive to create ownership among the workforce in favor of the change and what it can achieve for the organization. This can be created through a leadership team willing to accept responsibility for the change in all areas they can influence or control. Ownership can be created and reinforced through the use of rewards or incentives. The incentives can either be tangible, in the form of financial compensation, or intangible, in the form of psychological camaraderie and a shared sense of destiny.

Assessing Culture

Almost all successful change management programs pick up intensity and speed as they come down to other lower levels of the hierarchy. This is only possible if the management has done their homework and assessed all attributes of the organization’s culture. Companies often assess culture too late and do not recognize the importance it carries. Through cultural diagnostics, organizations can prepare themselves for change, bring a number of major problems to the surface, define all factors that influence leadership sources and identify conflicts. These diagnostics help in the identification of core values, behaviors and perceptions across all levels of the organization.

In this chapter we further look at how to adapt to change and how to become better at operations.

Chapter 2: Understanding the Impact of External Economic Activity on Business Growth and Success

For people who are unaware of it, the economy is defined as, “the state of a country or region in terms of the production and consumption of goods and services and the supply of money.”

At a rudimentary level, the economy of a region or country can be defined as its ability to generate and produce money. Before we study the impact of economy on businesses, we will first take a look at how the economy dictates behavioral spending patterns among consumers in a society.

Economic Growth Affects Government Spending and Policymaking

First and foremost, the economy around us affects just how a government acts and behaves. Economic growth plays a necessary part in stimulating business growth and spending. Increased exports and imports usually lead to greater income for businesses through business taxation. In simpler terms, governments get to have an improved cash flow due to an increase in business performance and revenue generation abilities. Once the government generates higher taxation, it eventually leads to higher government spending. Essentially everyone benefits from the process, as organizations can then push the money they earn into different services such as healthcare and other public provisions.

On the flip side, an economic recession or periods of low business revenue generation can reduce government spending and revenue generation. Governments start austerity campaigns and cut down on public expenditures to remove deficits. As a result of this reduced government expenditure and revenue generation, government services and provisions can fall into disrepair and suffer a lot. From healthcare to public transport and road repair, areas that require government funding and spending can reach a stagnation point. The standard of life reduces as a result and the government provisions in the region are neglected.

Public Infrastructure and Services are affected

As we have briefly mentioned in the point above, the economy directly impacts services and public infrastructure. During an economic recession, spending on the general public is reduced by the government. The impact further trickles down as businesses and the general public do not have the buying or purchasing power that they previously had.

Public services and infrastructure are the first to bite, with austerity in the following measures:

• Transport

• Healthcare

• General Maintenance

As a result of government austerity measures, public transport such as trains, trams and buses can experience reduced services and productivity. Moreover, private as well as public businesses do not have enough to spend on renovations, maintenance and new capital products. Healthcare is the first to stagnate during an economic recession. Due to limited resources and a lack of funds, the public may have to wait for longer durations for basic medical treatments and extensive surgeries and operations.

Aside from just this, the general maintenance of existing public goods could decrease as well. This could eventually lead public facilities into disrepair with deteriorating roads. Economic growth can lead to a contrasting situation as it helps improve transport, maintenance and healthcare across the board to boost public satisfaction and other related factors.

Cost of Living Will Fluctuate

For the general public, the main impact of economic fluctuations is felt in the cost and standard of living. The economic conditions in a society have an almost direct impact on the spending ability of our masses. An economic recession can lead to an increase in the cost of living and a drop in the general standard of living. Businesses are also strong armed into increasing their prices as they have to factor in for the growing cost of different raw materials and labor charges.

During periods of recession, the general public expects businesses to reduce prices for improved sales, but the improved revenue wouldn’t be of much use if it comes at a loss. During a period of recession, businesses often have no other alternative than to just increase their prices to make up for the increase in basic costs and the shortfalls in sales and turnover. For instance, a producer of luxury goods, for instance luxury cars, will have to increase prices further because sales volume would definitely be down as compared to what it was previously. People often cut down on their expenditure toward luxury goods during a period of recession. As a result, sales volume for a luxury car manufacturer would be down, and they would have no other option but to make more from the few units they are selling.

The series of events mentioned above has a snowball effect and can make conditions invariably worse than what they are. The snowball effect created as a result of rising prices can lead to hyperinflation in the economy. Hyperinflation is an economic condition where the prices of simple goods reach ridiculous levels – for instance, perhaps an exaggerate one, $10,000 for a loaf of bread. A region’s currency is bound to suffer due to hyperinflation and falls down the dumps. The decrease in currency rates also contributes to the inflation of prices, as imports are now a lot more expensive in relation to the local currency.

During periods of economic growth and prosperity, the general cost and standard of living is either maintained where it is, or it slightly improves for the better. The cost of living remains the same because prices barely change, even during economic prosperity, but due to the growing success of businesses in the industry, businesses make better profits and are able to offer more to employees.

Wages increase for the better, and residents are able to afford a better standard of living.

The Value of Currency Fluctuates

We briefly mentioned the impact the economy can have on a region’s currency. As we have mentioned above, the currency of a region is directly impacted by the economic change in the region. A strong economy more often than not leads to a stronger currency. On the contrary, a weak economy leads to a weak currency. What this means is that the national currency of a country does not have the same buying power in the international market.

For instance, a recession in the United States will lead to a drop in value for the United States dollar. This eventually means that your USD will be able to buy a lot less than what it can right now, when trading with other international currencies. For businesses in the host country, the falling forex rates have a direct impact on profitability and import and export processes. The general public will witness a steep rise in their international purchases, along with the money they have to pay while traveling.

Varying Quality of Life Standards

All of the impacts of changes in economic conditions that we have discussed above eventually go on to directly impact the quality of life in a region. Students for instance would have to work odd jobs to chip in with parents to manage finances. Times of economic recession can be hard on individuals and require everyone to up their game and step up where they can. The standard of living will drop as students have to focus on things other than just their school work and help their parents out in responsibilities that do not really fall under their expenses.

Moreover, the economy can also directly impact the disposable income of a family and the quality of life they enjoy. The quality of life most definitely declines during a recession, families do not have the resources to fund luxury purchases and other necessary equipment at times as well. Alternatively, periods of economic growth signal improvements in the quality of life. Life becomes a lot easier for families to afford luxuries that were previously unavailable to them, such as new electronics and holidays.

The question for all individuals without a relevant background remains, how does the economy actually affect the society around us? How does economic behavior change the way we behave in and live our lives? How does it change the way businesses operate and make growth plans? The economy changes from time to time, how does that dictate the innovation and flexibility that businesses today are required to show? These are all questions that we will look to answer through this chapter.

Chapter 3: How to Set Objectives for Your Business

In the literal sense of the word, a business objective means something you aim for. It is a goal or an end result that businesses today endeavor to achieve. While goals can be defined as short-term endeavors, objectives last for a longer time and set a long-term aspiration for businesses to follow. Goals could include weekly productivity expectations, monthly sales total or some other short-term objective based on instant results. Goals are essential for businesses, because they help with micro-management and form the roadmap that businesses can follow for success with objectives.

On the flip side, an objective means a long term path for business success over an extended period of time. Objectives are defined as what an organization aspires to achieve over a year of operations. The year itself is broken down into innumerable goals that lay the building blocks to achieve the objectives that businesses have.

Business objectives set a destination for organizations today. As individuals, we usually don’t hop into the car unless we know where we have to go. The same principle applies to business objectives. These objectives act as your destination, the place you want your business to reach. Individuals on executive levels can break down business objectives on a personal level as well to plan their own routine and activities in a way that helps the business achieve objectives. Every objective is unique to every organization, and managers can break them down to achieve an enhanced level of synergy across all sectors and hierarchies of the organization.

Economic Objectives

Economic objectives refer to the objective of profit generation and increasing revenue with time. All other objectives which are tied down to the generation of profit are also covered under economic objectives. The objectives businesses set as part of their economic growth include:

Profit Generation

Profit is the lifeblood of all businesses today. No business can survive in a competitive market without a free flowing stream of profit. In fact, most business entities today operate with the primary objective of profit generation – this is why they were brought into existence in the first place. Profit is earned to ensure the survival of businesses in a tough economy and to ensure positive expansion and growth over time.

Profits help businesses not only establish a positive income stream, but also expand their business and give stakeholders the returns they require. Businesses set other objectives as well that come under economic objectives in order to increase their profits.

Creation of Customers

Creation of new customers is another strategic economic objective that businesses have in mind today. A business unit cannot survive today unless they have new customers to buy their products and services. A business unit can only generate revenue and earn profits when it provides quality goods and services at prices that are reasonable. This can only be done through marketing efforts that attract new customers and sell more to the existing ones as well. Product quality, customer service quality and marketing activities play an important role in this objective.

Constant Innovations

Innovations are improvements that update the service or product standard offered to customers.

Innovations can even be related to the production process or to the distribution of goods to customers. The ultimate aim of an innovation should be toreduce wastage and reduce costs for better results. Business units can work on innovation to reduce costs and adopt better production methods for better results. Businesses are eventually able to increase their sales and revenue by attracting a lot more customers than usual.

Regular innovations and efficiency optimization can help achieve a number of objectives for businesses today. Reduction in cost, achieved through innovations, can help increase profit for the business. There are numerous cases of innovations in the business world today, which were achieved through the drive to optimize productivity and become more efficient.

Optimized Use of Resources

A business can only be run when managers have sufficient funds or capital. The amount of capital invested in the business can be used to procure machinery, employ labor, buy raw materials and generate cash to meet the daily operating expenses. Thus, business activities are a result of numerous resources like materials, machines, money and labor.

The availability of these resources, however, is usually limited. Thus, every entrepreneur should learn how to take calculated risks directed toward the best possible use of these resources.

Why Objectives Matter

A business can never succeed in a competitive market, without knowing what it wants. Most entrepreneurs and managers today fail at setting objectives for your business. Sure, they start well with a solid business idea and plan of implementation, but without a clear idea of where you’re headed or what your objectives are, businesses can stall before they even get running.

Regardless of the industry a business is in, business objectives and goals are necessary to find success. Objective setting and planning is one thing that remains constant or increases in importance with the passage of time. You can’t let go of the process or your objectives as you grow over time. In fact, these objectives become even more important as your business grows because there is more room for you to fail.

We look at all other kind of objectives as well in this chapter and study them in great detail.

Chapter 4: Metrics for Measuring Business Success

The metrics and the KPIs you choose for your business should ultimately help you achieve your objective. Completely unrelated metrics can give you a false sense of security, while your business diverts from the actual objectives it has set out for itself.

Start the progress by studying high level metrics that are crucial to the success of your business. Such metrics include net income or days to close. These metrics can then be followed up with a series of KPIs that help your team improve performance and become a more potent workforce. Successful KPIs help businesses track progress and monitor efficiency.

Metrics That Every Organization Should Track

What’s the best way to measure your business’s performance? Well, while there are multiple correct approaches and metrics for the job- one way not to do it is by following your gut. Running a business requires thorough understanding of the sales and financial results your business is able to achieve and an in-depth look at what can be done to better them.

This process of improvement cannot be implemented without the incorporation of relevant metrics that help in the tracking process. Your metrics should make tracking easier for you, and ensure that you are able to not only monitor, but also work on your performance.

In this section we explore a number of business metrics that are popularly used by businesses to explore company performance and to track your output. These metrics are discussed in greater detail, along with many more in the actual course manual.

Sales Revenue

Sales Revenue is an important performance metric and is by far the one you should always have your eyes on. We choose to have this metric mentioned right at the top, because it tells a lot about your company and the progress you’ve made or are capable of making.

Net Profit Margin

The net profit margin basically helps indicate just how efficient your company is currently at generating profits in comparison to the revenue generated. Most business owners evaluate their performance based on the revenue figure alone, without computing for net profit. Even when they do consider net profit, they look at both these figures in their individuality, without contemplating the impact they can have with regards to one another.

Gross Profit Margin

The gross profit margin is computed in a similar manner to that of the net profit margin, with the only difference being in the values of the profit considered. Taking the example we mentioned above forward, let’s say the manufacturer has a gross profit of $60,000 against the $100,000 of sales. The gross profit would be calculated by dividing it by the total sales revenue and multiplying by 100 if you want the answer in percentage. Your gross profit margin can be improved by adding efficiency to your production and sale processes. The more efficient you are in these two processes, the more profitable your business will be.

Sales Growth Year-to-Date

Similar to other profitability metrics, you can improve how you perform on this metric by working on your marketing and sales activities. Sales growth can also be boosted through marketing efforts that help give you the coverage you need across different platforms.

Cost of Customer Acquisition

The cost of customer acquisition can be improved by working on product or service quality and ensuring positive reviews and word of mouth marketing from current customers. This will help market your product or service naturally and will further help bring in new customers without spending lavishly on marketing processes. Also, referrals and recommendation processes can be implemented here.

Customer Loyalty and Retention

The results you get through this formula will help determine the number of customers that are loyal to you. The customer loyalty or retention ratio can be significantly improved through excellent customer care services and by delivering the highest quality of services to your customers. Consistent quality complemented with good customer service can help give your customers the motivation they require to stick with you.

Net Promoter Content

This metric is related to marketing and can be measured on a ten-point scale by conducting interviews and customer surveys. All customers with a rating of 8 or more can be considered promoters. Those coming in between 5 to 7 can be considered passive and those below 5 can be considered detractors. The data or substance for this ranking system is gathered through emails or customer surveys. The evaluation and data structuring process will take some time, but it will eventually give you enough leverage to rank your customers in a manner that you want. The net promoter score can eventually be found out by subtracting the percentage of detractors from the total percentage of promoters.

Your customer loyalty and net promoter score can be improved by enhancing your customer services and by delivering the quality standard that your customers expect from your brand.

Chapter 5: Evaluating Business Performance in the Modern Economy

Once their business is well set and running well, many entrepreneurs may feel inclined to let things continue in the same manner as before, without changing much about the processes that are performed at the core of the business.

However, initial success and customer traffic shouldn’t be taken as an indication to slack off. As soon as your business finds its initial footing, you should start planning again and reviewing your progress. After the crucial initial period has passed, you should regularly review the progress you make as a business and identify opportunities that can help you make the most of the position you find yourself in in the market. Entrepreneurs need to constantly evaluate their business and find new areas where they can take their business. As part of this strategy, entrepreneurs will even have to go back to their business plan and update it to match their current requirements. All developments you’ve noted should be strategically overseen and plans ready to counter threats.

This chapter takes you through the very important process of planning for your business’s success. Progress is a constant part of operations for all businesses by all means today and shouldn’t be compromised on at all. This guide takes you through the evaluation process and also suggests actions and processes that can help you through it.

Importance of Evaluating Business Progress

It is easy for entrepreneurs and managers to get overwhelmed by the day to day operations of their business and focus only on the current operations, without worrying about what the future holds. Once a business is up and running, it can pay dividends for entrepreneurs to think about strategic plans for the long-term. The importance of evaluation and progress becomes even more important as you take in more staff, appoint managers, create departments within the organization and become distanced from the usual everyday running of your business.

Reviewing your business’s progress can be particularly helpful if you feel:

• Uncertain about just how your business is performing and aren’t sure about what to do. This uncertainty can more often than not land businesses in hot waters.

• Unsure whether or not you’re getting the best possible output from the resources you have invested in your business. The possibilities here are endless and you should ensure you get the most out of your opportunities.

• Your business plan is out of data and needs serious updates. This can be true if you’ve been in business for over a year and still haven’t touched or considered your business plan in full.

• Your business is headed in the right direction. This question comes to mind when you’re sure of which direction you want your business to go in, especially with regards to a few metrics. You should always track business progress and determine whether it is in line or contrary to the direction you had set.

• The business is not responding to market demands in a manner that it should.

Evaluating progress can also come in handy if you have decided to take your business to the next level as far as output and operational efficiency are concerned.

Strategizing as Part of Business Evaluation

Strategizing is an important part of business evaluation as it gives you an opportunity to determine what’s right for you in the long run. Questions you can ask yourself while setting the strategy for your business include:

• What is the direction I want for my business? To determine the right answer to this question, you need to look at where you currently stand, where you see yourself over the period of the next three to five years, and how you plan to reach the end goal you have in mind for yourself.

• What are the recommended markets for your business now and in the future? Which markets should you step into, how will they change what you do and what your business needs to do to be involved in these multiple sectors?

• How can you gain market advantage? How can your business perform better than the competitors you currently have in the market of your choice, identified in the question above?

• What resources do you require to succeed in the modern economy? What skills, technical knowledge, relationships, finance, assets and managerial facilities and competence do you require to compete in the global market? Have these requirements changed since you started?

• What is the business environment that you’re currently part of? What external factors have a role to play in affecting your business’s ability to grow and compete?

• How can you measure the success of your organization? Remember that all measures of performance will change as your business matures and grows in stature.

It is doubtful for entrepreneurs to be able to answer these questions on their own, which is why they can involve their advisors and other trusted personnel to come up with reasonable answers.

This chapter will take a look at the different methods for strategizing in the business economy today and how they work well for different businesses.

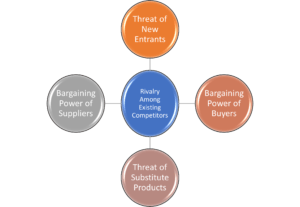

Chapter 6: Porter’s Five Forces

Porter’s Five Forces is a framework used to analyze the level of competition within an industry and determine just how that competition impacts you and your business. The five forces can prove to be especially useful when businesses are starting fresh, or are thinking of joining a new business.

According to Porter and his five forces, the competition in a certain industry comes through a number of factors, other than just the competitors themselves. Porter believed that the state of competition in an industry is dependent on a number of factors, including the threat of new entrants, the bargaining power of suppliers, the bargaining power of buyers, the existing industry rivalries and the threat of substitute products or services.

The collective strength of all these forces together helps determine the profit potential of an industry and what it means to the average business. If all of these five forces are intense, as is the case with the airline industry, then almost no company in the industry will be able to earn attractive returns on their investment. However, if the forces are mild, like is the case in the soft drink industry, then there is significant room for higher returns and interest rates.

We will elaborate on each force in this chapter, with a concurrent example of the airline industry to build concepts further. The airline industry gives a helpful blue print to understand all forces of the analysis and will help better understand and comprehend the situation.

We conduct our analysis by discussing a few factors affecting each force outlined by Porter along with a guide on how businesses can use this analysis. With this done, we will move on to discuss each force in detail and illustrate it further through an example from the airline industry. You can reach out to the course manual to read all this.

Ways Porter’s Five Forces Can Help You Succeed in Business

Most business owners and managers spend their whole careers thinking of competitive forces that can shape strategy. The competitive forces in most industries aren’t static, which is why routine analyses of your industry are vital for success.

Porter’s five forces help in this analysis by adding value in the following stages:

When You Start a Business

Before you take the leap of faith into an unfamiliar industry without prior knowledge of what works and does not work in the industry, it is necessary that you run and understand Porter’s five forces analysis in full to get the lay of the land.

Understanding the factors covered in the five force analysis can be necessary for success later in your business life. Be realistic about the stability in the market and also determine how new entrants can influence your market share.

When You’re Evaluating Profit Potential

Porter’s five forces can be the go-to solution to evaluate the profit potential of your organization and find where you stand with regards to profitability and success. The five force analysis can be an excellent way to get an accurate picture of what the future holds for you. As a business owner, it is necessary that you stay up to date with how the industry is changing and implement the dynamic solution of Porter’s Five Forces. Make sure that all decisions are based on accurate information.

When You’re Determining the Efficacy of a Strategy

Porter’s five forces analysis can help you determine the effectiveness of a strategy after it is completed. The analysis will help give you results and updates on whether the strategy worked or not and will also help guide you forward in your future endeavors.

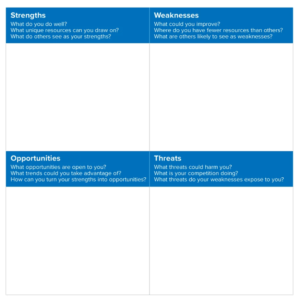

Chapter 7: SWOT Analysis

A SWOT Analysis is an analysis tool that helps asses four of the key aspects of your business; Strengths, Weaknesses, Opportunities and Threats.

Businesses today can use SWOT Analysis to determine their current standing and to get an idea of future growth potential. Better still, organizations and managers can use the platform to craft actionable strategies for the future that help distinguish them from the competitors in the industry.

Strengths

Strengths are all the things that your organization does particularly well, or better than the competition in your market. In a way, your strengths should distinguish you from your competition and make you stand out as a quality provider. When you’re thinking of strengths, it is nice to brainstorm and think of all the advantages that your organization has over other organizations in the industry. These advantages can work as factors to motivate your staff forward. The factors can include better staff skill set, better managerial expertise, strong set of manufacturing processes, use of quality supplies and materials among much more.

Weaknesses

Weaknesses, similar to strengths, are inherent features found within organizations. As part of these weaknesses, you should focus on the inherent features of your organization and the people, resources, procedures and systems involved in your workplace. Think about all the areas of your workplace that you would like to improve and the sort of practices you should realistically avoid to improve these areas.

Opportunities

Opportunities are all chances and openings that signal some positive event is about to take place. Opportunities are an important part of the SWOT analysis, as they help determine the future feasibility of your organization. Organizations need to monitor opportunities in a consistent manner to gather some fruit for them and to ensure that they reap the results that organizations expect from them.

Threats

Change is by far the only constant in the world of business, and if you’re not adapting to new technologies and production practices, then your growth will eventually stall and you will fall prey to the innovation in the market. The ever evolving technology standards around us are an ever-present threat, which require organizations to continuously update their processes for the better.

Chapter 8 Root Cause Analysis

Business analysis methods, as tricky as they may sound, can often be understood through real life examples related to them. The simplest and by far the easiest way to understand root cause analysis is to think of it through the outlook of common everyday problems. Imagine you’re sick and throwing up at your workplace, the best thing to do is head over to a doctor and find out the root cause behind your sickness. If your car stops working all of a sudden or develops a problem, the best course of action would be to head over to a mechanic and have them inspect the vehicle to unearth the root cause of the problem.

In both cases above, an expert with an understanding of problems in the relevant niches will help direct you to the root cause of the problem in your body or in your car. Similarly, if your business is not performing in the manner you want, a root cause analysis will find the primary reason behind the dip in performance and provide solutions to it.