Client Retention Strategy

The Appleton Greene Corporate Training Program (CTP) for Client Retention Strategy is provided by Mr. Weimer Certified Learning Provider (CLP). Program Specifications: Monthly cost USD$2,500.00; Monthly Workshops 6 hours; Monthly Support 4 hours; Program Duration 12 months; Program orders subject to ongoing availability.

Personal Profile

Mr. Weimer is an approved Certified Learning Provider (CLP) at Appleton Greene and has experience in Client Retention, Sales and Management. He received his Bachelor’s of Business Administration from Duquesne University and his Masters of Health Service Administration from Gannon University. Having been trained in sales and account management within the pharmaceutical industry he started to focus on his passion around strong client retention. While the Director of Client Retention for Syneos Health he was able to increase retained revenue by implementing the Clients for Life® client retention process by over $300,000,000.

In 2017 Mr. Weimer became a Partner in a leading client retention company, and as Partner, he expanded his knowledge base. Mr. Weimer has successfully retained revenue for his many clients in the following industry sectors, Pharmacy Benefit Management, Revenue Cycle Management, Specialty Pharmacy, Advertisement, Facilities Management, Information Technology and Healthcare suppliers.

Following his success as a Partner, he later became the Principal Partner and Chairman. Today Mr. Weimer Overseas the companies work in the United States, Canada and Europe. His goal is to continue to provide the same outcomes he has achieved for Tenacity’s Clients by enhancing the principles he first used as the Client Retention Director and Principal Partner of the firm by incorporating his learning, research and experience to create a world class client retention process.

To request further information about Mr. Weimer through Appleton Greene, please Click Here.

(CLP) Programs

Appleton Greene corporate training programs are all process-driven. They are used as vehicles to implement tangible business processes within clients’ organizations, together with training, support and facilitation during the use of these processes. Corporate training programs are therefore implemented over a sustainable period of time, that is to say, between 1 year (incorporating 12 monthly workshops), and 4 years (incorporating 48 monthly workshops). Your program information guide will specify how long each program takes to complete. Each monthly workshop takes 6 hours to implement and can be undertaken either on the client’s premises, an Appleton Greene serviced office, or online via the internet. This enables clients to implement each part of their business process, before moving onto the next stage of the program and enables employees to plan their study time around their current work commitments. The result is far greater program benefit, over a more sustainable period of time and a significantly improved return on investment.

Appleton Greene uses standard and bespoke corporate training programs as vessels to transfer business process improvement knowledge into the heart of our clients’ organizations. Each individual program focuses upon the implementation of a specific business process, which enables clients to easily quantify their return on investment. There are hundreds of established Appleton Greene corporate training products now available to clients within customer services, e-business, finance, globalization, human resources, information technology, legal, management, marketing and production. It does not matter whether a client’s employees are located within one office, or an unlimited number of international offices, we can still bring them together to learn and implement specific business processes collectively. Our approach to global localization enables us to provide clients with a truly international service with that all important personal touch. Appleton Greene corporate training programs can be provided virtually or locally and they are all unique in that they individually focus upon a specific business function. All (CLP) programs are implemented over a sustainable period of time, usually between 1-4 years, incorporating 12-48 monthly workshops and professional support is consistently provided during this time by qualified learning providers and where appropriate, by Accredited Consultants.

Executive summary

Client Retention Strategy

The preservation of clientele holds paramount importance for any establishment, yet the dedication and effort given towards client retention often fall short. This translates to a substantial impact on the financial standing of the company. The significance of retaining clients is particularly pronounced in the realms of business-to-business interactions and service-oriented sectors. Each client has the potential to contribute significantly to the overall revenue stream, with a select few clients sometimes accounting for well over 80% of the total realized revenue.

Acquiring each client may have entailed a prolonged period, spanning months or even years. The sales cycle is protracted, consequently elongating the duration required to recover the initial investment. It would be disheartening to lose hard-earned clients due to insufficient attention and effort directed towards maintaining those relationships diligently cultivated over time.

In the business-to-business domain, client relationships are not as transient as in the direct-to-consumer landscape. Merely implementing a loyalty program or advertising campaign is insufficient. A more comprehensive approach is imperative. Within the service sector, the significance of a brand name and reputation has diminished compared to the past. With the proliferation of so many touchpoints, competitors can swiftly engage and influence your most valued clients, posing a substantial threat. Previously, relationships alone may have sufficed to retain clients, but in the contemporary business environment, this is no longer the case.

Traditionally, corporations have predominantly focused on sales and business development. However, the revenue impact generated by sales efforts pales in comparison to the potential of a robust client retention strategy. The cost of acquiring a new client is five times higher than retaining an existing one, yet most companies allocate most of their resources to client acquisition, relegating client retention to a secondary priority. The adage “wins are celebrated in the boardroom, while defeats are murmured around the water cooler” rings true, despite numerous studies demonstrating that a mere 5% enhancement in client retention can yield a profit increase of 25% or more, offering unparalleled returns on investment.

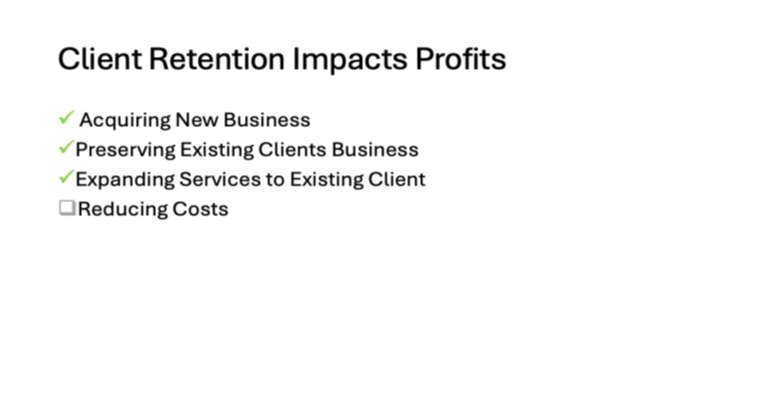

Essentially, there exist four primary avenues to influence revenue generation. Firstly, by acquiring new business; secondly, by preserving existing clients; thirdly, by expanding product/service offerings to current clients; and lastly, by reducing costs. A robust client retention strategy impacts three out of these four avenues. Enhanced sales stem from quality referrals, extended client retention periods, and improved product/service offerings tailored to meet the evolving needs and expectations of current clients. Although client retention does not directly reduce costs, a modest 2% increase in client retention can have a more substantial impact on revenue than a 10% cost reduction, making client retention a more favorable option.

The repercussions of client retention extend beyond revenue implications. A decrease in clientele translates to reduced resources available for servicing remaining clients, potentially leading to client dissatisfaction. Dissatisfied clients are less likely to provide referrals or may even offer negative feedback, impeding growth. Slower growth triggers operational strain within the company, fostering employee discontent. This cyclical pattern engenders a negative organizational culture that is detrimental to long-term success.

Current Position:

It is a common practice in the business realm to establish fundamental elements and label it as a client retention strategy. Initially, an account management team is typically assembled, followed by the adoption of a Customer Relationship Management (CRM) system. The notion prevails that monitoring client data and engagement activities constitutes a robust client retention strategy. Subsequently, a survey or Net Promoter Score (NPS) assessment is frequently administered, under the assumption that a numerical representation signifies content and loyal clientele.

However, despite these efforts, unforeseen occurrences may arise, such as the abrupt departure of a major client without prior notice. Astonishingly, a large percentage of clients opt to silently disengage without even letting you know. They just walk away. This unexpected turn of events often leaves leadership bewildered, subsequently requiring them to justify to stakeholders the oversight of such a significant impact on the company’s financial performance.

Implementing basic components and leaving client retention to chance proves inadequate. While these elements hold significance, they do not constitute a comprehensive and formalized client retention strategy. A more intricate approach is imperative to avert receiving distressing notifications that could jeopardize revenue forecasts for the entire fiscal year.

Effective account management necessitates structured guidance and rigorous training that has demonstrated efficacy and outcome-driven results, akin to the training provided to the sales team. Generic training programs fall short in preparing account managers to spearhead a proficient customer-facing team that not only comprehends but surpasses client expectations. Without adequate training, Quarterly Business Reviews (QBRs) risk devolving into mere data presentations, rather than strategic sessions focused on surpassing expectations and fostering innovation.

Account Teams are currently missed their client’s key expectations. It is sad that 80% of account teams believe they are delivering superior service while only 8% of clients believe the same thing (Bain & Company). We must do better to close this chasm. We also need strong relationship on multiple levels. The network now is often one dimensional.

While CRM systems play a pivotal role in client retention strategies, they are merely tools. These platforms serve as repositories for tracking activities, relationships, strategies, accountability, and service/product execution. Without customization and a deliberate framework, CRM systems risk becoming underutilized investments that fail to enhance client retention rates. A CRM is there to support a strong client retention strategy. It is not the strategy in and of itself.

Furthermore, while surveys offer valuable insights into client satisfaction levels, they do not consistently correlate with client retention rates. Evaluating the sentiments of key stakeholders with decision-making authority holds greater significance than survey results alone. A holistic approach encompassing various facets is indispensable for sustained client retention.

Historically, the efforts of current clients have often fallen short. Organizations that have embraced comprehensive client retention strategies have witnessed tangible outcomes, including substantial revenue preservation, enhanced reputation, client retention, and expansion of service offerings. The paradigm is gradually shifting towards proactive initiatives aimed at bolstering client retention rates. The cost of neglecting or just giving a nod to client retention is just too great!

Future Outlook

Our approach revolves around leveraging more than 38 years of expertise in molding and nurturing optimal strategies in client retention, resulting in the creation Tenacity® Incorporated’s Clients for Life® client retention process. Clients for Life represents a proven, structured client retention approach that has consistently demonstrated remarkable outcomes. The full adoption of Clients for Life yields a substantial return on investment. This client retention process is a meticulously crafted approach that centers around three fundamental pillars: Assess, Create, and Execute, each encompassing crucial elements essential for successful implementation.

The initial step entails a thorough Assessment of both the internal strategy and capabilities of your organization, alongside understanding your clients’ perceptions and pain points. Ideally conducted by an impartial third-party observer, this comprehensive internal evaluation is complemented by an assessment of key clients contributing significantly to your revenue, encompassing those who are advocates, neutrals, and critics. When completed you will have a strong understanding of both your internal capabilities as it pertains to client retention as well as your clients’ perceptions. This transcends mere qualitative surveys or momentary client satisfaction scores, providing a profound insight into your company’s standing and paving the way for the creation of a comprehensive client retention strategy.

Moving on to the second step, the act of Creating a strong client retention strategy must be entrusted to the leadership team. It is imperative that leadership actively participates in shaping and advocating for the client retention process, as their commitment sets the tone for the entire organization. The organization is looking to see the importance you are putting forth in client retention. A successful implementation involves celebrating client renewals and expansions with the same fervor as new business acquisitions, identifying the right clients under suitable terms, sharing insights gained from past setbacks, and crafting a client journey that ensures seamless onboarding and renewal. The Chief Information Officer (CIO) plays a pivotal role in outlining a roadmap for a robust client retention platform that ensures accountability, thereby establishing a solid foundation for the subsequent Execution of the client retention strategy. Leadership will have the benefit of all the years of experience Mr. Weimer and his firm brings to the table along with the principles and fundamentals of the Clients for Life® client retention process.

The final step necessitates is the execution of the formalized strategy, commencing even before the prospective client is onboarded. Collaboration between sales and Operations is crucial to surpassing expectations, delivering impeccable service to clients, safeguarding the company’s interests, and fostering robust connections between your organization and the client. This strategic approach not only tackles current challenges but also paves the way for future innovations, ensuring sustained growth and a lasting relationship.

Upon successful implementation of the Clients for Life® client retention process, a minimum increase of 5-10% in client retention rates can be expected based on our extensive experience. The track record of success following the full integration of this process speaks for itself, highlighting the transformative impact a well-crafted client retention strategy can have on a company. Ultimately, the key lies in leadership’s unwavering commitment to the implementation of a formalized process.

Curriculum

Client Retention Strategy – Part 1- Year 1

- Part 1 Month 1 Executive Introduction

- Part 1 Month 2 Executive Assessment

- Part 1 Month 3 Executive Strategy

- Part 1 Month 4 Executive Execution

- Part 1 Month 5 Retention Platform

- Part 1 Month 6 Operations Introduction

- Part 1 Month 7 Operation Insights

- Part 1 Month 8 Understanding Expectations

- Part 1 Month 9 Understanding Relationships

- Part 1 Month 10 Solving Problems

- Part 1 Month 11 Training Trainer

- Part 1 Month 12 General Training

Program Objectives

The following list represents the Key Program Objectives (KPO) for the Appleton Greene Client Retention Strategy corporate training program.

Client Retention Strategy – Part 1- Year 1

- Part 1 Month 1 Executive Introduction It is crucial that the C-Suite fully commits to understanding and implementing a strong client retention process. This process has a direct impact on increasing sales, retaining revenue, and growing from within. By committing to client retention, a company can significantly reduce the need to cut costs. Setting clear goals and establishing baselines is the first step in implementing a successful client retention process. Once goals have been set, it is important to review and understand the key principles of a proven client retention process, such as the Clients for Life® client retention process. Assessing your business both internally and externally is essential in understanding where your company stands in terms of client retention. Conducting a Capabilities Assessment and engaging in objective conversations with key clients will provide valuable insights. A FreshEyes® Review report will help identify areas for improvement. Creating a strong client retention strategy is a task that only leadership can undertake. By focusing on concepts such as Right Clients/Right Terms®, Lessons Learned, Warning Signs, and the Client Journey, a solid strategy can be developed. The final step is to execute the client retention process. This involves setting clear expectations, utilizing the Web of Influence, and delivering for clients today while also innovating for the future. By following these key concepts, a company can effectively retain and grow its client base. Overall, commitment from the C-Suite is essential in implementing a successful client retention process that will benefit the company in the long run. By following the key principles and steps outlined, a company can create a strong foundation for growth and success.

- Part 1 Month 2 Executive Assessment Why focus so much on Assessment? First, a comprehensive review is needed to comprehend your company’s strengths, weaknesses, and views on client retention. The results of the Capabilities Assessment that was introduced in the Executive Introduction will be shared. This will also set a baseline moving forward. Second, understanding how your clients perceive the value your company provides is a great predictor of your company’s ability to retain and grow the business. Most clients do not leave because of the prices of your services. They leave because of the perceived value you are providing today and your ability to grow and adapt with them in the future. Often a client’s perceived value is done by reviewing client surveys and Net Provider Scores (NPS). There is a benefit in understanding a rating of how your company has performed in a snapshot in time with a survey. It is just not enough. Studies show there is no correlation between NPS and client retention. For client retention, a more robust qualitative approach needs to be done. This is the reason for the FreshEyes® Reviews. During the Executive Assessment, a first read will be given on the output of the FreshEyes® Reviews on the key clients identified. We will review how to review and respond to the FreshEyes® Reviews and the importance of setting up standard operating procedures. The capabilities assessment and the initial FreshEyes® Reviews will be a good start to truly understanding your company’s approach to client retention. However, two or three companies do not reflect a trend. It is enough to get started but a larger sample size is needed to uncover trends. For this Tenacity has developed Common Threads/Common Threats. The concepts and process of the Common Threads/Common Threats will be reviewed, and additional clients will be identified for FreshEyes® Reviews. Together the internal and external assessment, along with a better understanding of what is needed to Assess your current business, will position your company well moving forward.

- Part 1 Month 3 Executive Strategy Once there is a clear understanding of the impact of client retention on your company and your strengths and weaknesses, it is time to create a strategy specific to your company. This starts by forming your Partner Success Team. This will be a cross-functional group of individuals who oversee the implementation of the Client for Life® client retention process. Key individuals from Operations, Sales, Information Technology Finance, and Analytics should be assigned to the team. The team will also have an executive sponsor to ensure success. This team will also show the executive team’s commitment to client retention. In addition to a Partner Success Team, companies often assign a Client Retention Executive with a direct line to the CEO. It is incumbent on leadership to set the tone, guidance, and mentorship as well as structure. This will be accomplished by defining the Right Clients/Right Terms, lessons learned, warning signs, and client journey. The executive strategy session moves from concept to action. The Partner Success Team will establish the right clients for your company to have as clients under what terms. Too often companies accept all clients on almost any terms causing resources to be pulled from the clients that have the potential to grow your revenue far into the future. It is also the responsibility of leadership to share the experiences from the past. Future losses can be prevented by sharing how and why past losses occurred. There are usually a handful of reasons that if highlighted can avoid losses in the future. The Lessons Learned will be accompanied by the warning signs. Finally, it is the responsibility of the Partner Success Team to review the current client journey and ensure that the process is well-defined and supports the client from the verbal agreement forward. The Executive Strategy session is the executive team’s opportunity to put their imprint on the client retention strategy through the Patient Success Team and the creation of key guidelines and learnings from the past.

- Part 1 Month 4 Executive Execution Everyone must understand and implement from the same playbook. This is the opportunity for leadership and the Partner Success Team to become familiar with the Execute principle of the Clients for Life® client retention process. This will allow leadership to champion and model the key concepts within the Execute principle. The first concept that will be reviewed is understanding your client’s expectations. Expectations are the measure by which clients determine success or failure. Therefore, we must know how expectations are created, the importance of relevant value, and how to ensure we capture and execute our clients’ expectations. The second concept is ensuring a strong network on both the company and client’s side of the relationship. A strong Web of Influence® is needed to ensure the relationship is strong and a change on either side does not affect the health of the account. A strong relationship must be anchored on trust. The key elements of trust will be reviewed along with the need to be a partner and not a vendor. This requires the ability to communicate effectively and with the correct tone. The third concept that will be implemented today will be planning and innovating. Providing technical support is a key factor in extending the relationship. First, you must do the job you were asked to do before you provide additional services. That said, a strategic plan must be in place to retain and grow each client. For the larger clients, a Team Account Retention Plan (TARP) will need to be implemented. After this training session, leadership will have the knowledge and the resources to kick off the client retention training for sales and operations.

- Part 1 Month 5 Retention Platform There is one more step before the client retention training is ready to be shared with the sales and operations team. A platform must be in place that can house all the key concepts previously reviewed. Without a platform accountability, communication, and planning will take a step back. The ideas will be shared but the implementation will wax and wane. Two options are possible to ensure a strong client retention platform is in place. The first option is to adapt and customize your current software system to incorporate the needed, fields and reports for the Clients for Life® client retention process. The benefit of this approach is to have a system everyone is used to using. The negative is that there is often a significant number of workarounds to accomplish the goal, and the output may not be exactly what is needed. The second option is using Tenacity’s platform. The benefit is all the fields and reports are available. While the Tenacity platform works with most major systems, it is not what the company has used in the past. Whatever choice you make we will walk you through the requirements, help you test and customize for your needs, and assure it is ready for implementation.

- Part 1 Month 6 Operations Introduction Now that the groundwork has been laid, it is time to introduce the formalized Clients for Life® client retention process to operation as well as sales. Done properly there should be a groundswell of excitement about client retention and how it will impact business going forward.

To launch the training to those customer-facing individuals that will determine the success or failure of your client retention strategy, the first introduction should be made by the CEO or someone in the C-Suite. This will show the importance and determination the company has in succeeding in all client retention expectations. The importance of client retention in the business will be shared through the lens of how a strong client retention process can positively impact their day-to-day lives. We will show the difference a strong client retention strategy has on not just profits but on operational stress and job satisfaction vs. a poor client retention strategy. The group will then start to internalize the importance by walking through case studies showing how strong client retention strategies have benefitted the relationships they have with their clients. Along with the case studies, we will go through the Capabilities Assessment that was reported earlier. This will show areas the company is doing well on client retention and areas that need improvement. After operations and sales have aligned on the importance we will go into the key principles of the Client for Life process. The key elements of Assess, Create, and Execute will be shared with the group along with a timeline on how the process will be rolled out. The participants will leave the session with excitement and determination on the path forward. - Part 1 Month 7 Operation Insights It is easy for those who deal with the client every day to start to have a biased view of how the client perceives the value of the work done. Unfortunately, there is a chasm between how the client views performance versus how the account team views performance. 80% of account teams believe they are providing superior service, but only 10% of clients think they are receiving superior service. How could this be? Often the closeness of the relationship or a misunderstanding of the client’s expectations can get in the way of a true assessment of the relationship. This is the importance of an objective 3rdparty assessment to get a fresh look at the relationship. The FreshEyes® Review importance and format will be reviewed as well as how to read and respond. The FreshEyes® Review should be seen as a tool and not a performance review. Judgement is left at the door. What is more important is how the company deals with the client’s perceptions. To summarize the objective portion of the Assess principle we will review the Common Threads/Common Threats will be reviewed to show trends both positive and negative. An action planning session will then take place to work towards a path forward. We will cap off the session with a subject review of their clients by completing a Client Health Assessment. This is a tool that is best reviewed by the entire account team to take a snapshot of the health of the relationship by reviewing communication, relationships, and expectations. Finally, standard operating procedures will be reviewed along with how assessment is addressed in the retention platform.

- Part 1 Month 8 Understanding Expectations Expectations are the cornerstone of increasing your company’s value in the eyes of your clients. They serve as the yardstick by which clients measure performance and are incredibly powerful. Yet, they often do not receive the attention they deserve. Expectations evolve over time as our experiences and the environment around us change. We will explore the relationship between euphoria and time. What was important to someone last year may not hold the same significance today. Expectations can be highly dynamic, requiring constant vigilance. Expectations are also highly individualized. What is crucial to one person may not be as important to another. We will discuss Relevant Value and its implications for business. To illustrate relevant value, we will examine the Golden Rule, the Platinum Rule, and the Diamond Rule. In essence, this involves viewing expectations through the lens of one’s own perceived value, the client’s perceived value, and the client’s perceived value of working with a knowledgeable professional. Once the basic concepts of expectations are well-understood, we will move on to implementing them. There is only one way to truly understand someone’s expectations: ask them. This must be done consistently throughout the client journey. It begins before the contract is signed and continues throughout the relationship. This process starts with the Transition Meeting, a formal handoff between sales and operations before the contract is signed. Expectations are then reviewed and updated at least annually in an Expectations Meeting. We will present a very prescriptive and proven process that has yielded results. Finally, we will cover Standard Operating Procedures and how the retention platform will be applied.

- Part 1 Month 9 Understanding Relationships In the service sector, a business relationship cannot merely be transactional; it demands a deeper investment in the quality and enduring nature of the relationship. Such a relationship must be dynamic and resilient through the highs and lows of business cycles. First and foremost, it is crucial to ensure a robust Web of Influence®. This involves creating a healthy network that is equally strong on both your company’s side and the client’s side. This network should encompass all levels of both organizations and include the necessary subject matter experts. We will then discuss the role of the account manager responsible for the Web of Influence®. The next step is to focus on the quality of the relationship, which hinges on a strong level of trust built upon Caring, Candor, and Competency. The objective is to elevate your status to that of a true partner, rather than just another vendor. Achieving this requires building a team that can communicate effectively and deliver substantial value to the client. The third step involves evaluating the necessary actions when changes occur on either side of the Web of Influence®. Changes in personnel can significantly impact the relationship. To mitigate risks, it is crucial to swiftly arrange a meeting with any new entrant to the relationship. This Transition Lite Meeting is an opportunity to review previously resolved issues, current expectations, and any new expectations the client may have moving forward. Finally, we will delve into the retention platform. This platform plays a significant role in the Web of Influence® and will be reviewed in detail, along with standard operating procedures. Its purpose is to ensure long-term client retention by establishing a consistent and reliable framework for managing relationships.

- Part 1 Month 10 Solving Problems Lastly, but certainly not least, we must ensure that your company is excelling in the tasks it was hired to perform. Fulfillment of the need that led to your hiring is crucial, and it is vital to either meet this expectation or be well on the way to doing so. We will examine the relationship between the complexity of the problems needing resolution and the fees being charged—a concept we will refer to as Revelation X. This term signifies the tendency for problems to diminish over time as they are resolved, while fees or business profits tend to increase. Eventually, these two will converge, creating a point where the fees surpass the remaining unresolved problems. This inflection point poses a risk of losing the business to a less expensive competitor or the client deciding to handle issues internally. At this juncture, a decision must be made: reduce the fees, or preferably, identify new problems that need solving through innovation. Revelation X should be viewed as an opportunity to grow with your client by partnering with them to innovate for the future, thereby easing their current challenges. To retain existing business and achieve future growth, a comprehensive plan must be in place. We will review the account planning canvas and outline the steps for implementing a successful Team Account Retention Plan (TARP) for larger clients. Finally, we will chart a path forward, as each account team takes inventory of everything learned through the Clients for Life process.

- Part 1 Month 11 Training Trainer The components of the Clients for Life® client retention process are now fully established for leadership, sales, and operations. The next step is to integrate this process seamlessly into your everyday business practices. To achieve this, the Partner Success Team and the Client Retention Executive must be prepared to train others and sustain the process over the long term. We will collaborate closely with the Partner Success Team to ensure they are equipped to train new hires and reinforce the essential concepts. The Partner Success Team should become subject matter experts in every facet of client retention. Our first step involves a detailed review of all materials to ensure complete understanding and confidence in conveying the information to others. Following this, we will observe and coach the team to meet the quality standards expected by Tenacity and your company. This will be accomplished by having the team teach us the Clients for Life process. We will also share best practices on how to effectively implement key principles and action items within Assess, Create, and Execute. A crucial part of achieving success is maintaining a high level of accountability, which is facilitated by the monitoring and reporting features of the client retention platform. You must inspect what you expect. The Partner Success Team, with our support, will devise an individualized timeline and strategy. Before the “train the trainer” program is completed, a comprehensive plan for the year following the launch will be established. In the end the Partner Success Team and the Client Retention Executive will have all the resources and confidence to move forward.

- Part 1 Month 12 General Training By now, excitement should be growing about our new focus on client retention through the Clients for Life® process. You’ll start to notice that employees outside of sales and operations are beginning to ask questions about terms that are circulating throughout the organization. It’s crucial to bring the entire company on board. Doing so will create a corporate culture dedicated to client retention. The Clients for Life® process will be condensed into a single session. While all aspects of the process will be covered, the information will be presented in a more generalized format, tailored so that each department can find value in it. It’s imperative that everyone understands the importance of implementing a robust client retention strategy. We will review the assessment phase to ensure everyone is familiar with the terminology and general findings. This includes examining the Common Threads/Common Threats and the Capabilities Assessment to provide insights into current trends. During the Create phase, we will discuss warning signs, so that every employee who interacts with clients, or has the potential to do so, can help alert the account team to any risks moving forward. When we reach the Execute phase, we will go over everyone’s role in establishing and fulfilling key expectations. Every employee who answers a phone call, replies to an email, or addresses a concern should understand the difference between The Golden Role, The Platinum Role, and The Diamond Role. Furthermore, every person in the company should understand their role in the Web of Influence® and be prepared to contribute to the company’s growth by staying vigilant for opportunities to innovate for clients. At this point, you have all the components needed for a stellar strategy to boost sales, retain existing clients, and achieve organic growth through innovation. While we will continue to be a resource moving forward, you now possess the tools required for success.

Methodology

Client Retention Strategy

Program Planning:

The journey towards long-lasting client relationships begins with the Executive Team. Their commitment to your client retention strategy is crucial as it sets the tone for the entire organization. By weaving client retention into every aspect of your operations, we can demonstrate to our clients that they are an integral part of our business.

Before setting the tone, the Executive Team must be aligned on the criticality of client retention. This involves a thorough evaluation of our current financial standing, understanding your clients’ perceptions, assessing your company’s capabilities, and forecasting the overall impact. Our proprietary insight and assessment tools will provide a comprehensive analysis of our client retention status.

Once we have a clear picture of your current client retention health, we can chart a path forward. Defining success in client retention is essential. Where do you want to be in terms of retention rate in one year? How will you define and measure retention moving forward? We will work closely with you to define these parameters and set the stage for success.

In planning for the future, we must determine who in your organization will be impacted and when training will take place. By investing in your people and providing the necessary training, we will equip your teams to deliver exceptional client experiences. We will help you identify the right individuals for training and develop a robust training schedule for the upcoming year.

As the Executive Team sets the tone, it’s crucial to develop a clear communication plan and lay out the next steps for the entire organization. This will ensure that everyone is aligned and empowered to contribute to our client retention objectives.

Program Development:

Now that the Executive team has established the tone and defined the goals for the organization, it’s time to craft a powerful strategy. The Partnership Success Team, in conjunction with the Executive Team’s guidance, will lead the charge.

Comprised of versatile leaders, the Partnership Success Team will spearhead and oversee the organization’s client retention strategy on all fronts. They will play a pivotal role in shaping key elements of your organization’s blueprint for a robust retention process, which will then be cascaded throughout the entire organization. The Partnership Success Team will provide valuable advice, coaching, and direction at each juncture of the client retention process and will be under the direction of the Client Retention Executive.

The Client Retention Executive will hold a full-time or part-time position and will bear the responsibility for the success of the retention strategy and its outcomes. This influential figure is likely to be a prospective senior executive who will dedicate their time entirely, or predominantly, to client retention.

During the program development phase, the Partnership Success Team and the Client Retention Executive will define the Right Clients/Right Terms for your company, impart learnings from past client losses, and highlight warning signs to avert future losses. They will also review the client journey to craft a customized strategy for your company. The team will look at every twist and turn in the client’s experience and ensure a seamless handoff along the way.

Upon obtaining executive approval, the Partnership Success Team will diligently work towards ensuring the seamless implementation of the Clients for Life® client retention process within the company.

Program Implementation:

It’s crucial that our customer-facing teams fully implement the Clients for Life® client retention strategy. This responsibility primarily falls on the sales and operations teams, and they need tailored training to effectively carry out the strategy developed by the Partnership Success Team and approved by the Executive Team.

A representative from the Executive Team will lay out the goals and emphasize the importance of a robust client retention strategy. They will also share the guidelines of the Right Clients/Right Terms®, along with Lessons Learned and warning signs, and outline the way forward.

While everything leading up to implementation is important, the adoption and execution of the strategy by customer-facing roles are absolutely critical. This group must not only meet expectations but exceed them, build a robust Web of Influence®, and tackle today’s challenges while preparing for the future.

Nothing will be left to chance. We will commence with comprehensive training on the concepts to ensure complete understanding and alignment. Workshops will be conducted for each concept and the team will work together to gain better insight on how the concept pertains to the way they do business. Then they will review each concept to create an impactful action plan moving forward.

Subsequently, we will conduct mock exercises to demonstrate successful execution of each concept. The group will leave the training with unwavering confidence and the necessary skills to execute the retention process. We will then collaborate with The Partnership Success to make sure that all that was asked for the group to do is capture in the retention platform.

Program Review:

We will start by thoroughly assessing the training, capabilities, and clients’ perceptions of your company, along with the defined retention rates. It’s essential to note that the Clients for Life® client retention process doesn’t culminate when the training is completed – it’s only the beginning. Once the training phase ends for existing employees, the implementation phase begins.

However, before progressing, it’s crucial to pause and evaluate the impact. This involves conducting another assessment of the capabilities of those previously surveyed. Have the capabilities improved over the baseline? Have we achieved a positive change, and what work remains to be done?

This is also the opportune time to conduct FreshEyes® Reviews with key clients previously interviewed, and to perform PostMortem Audits® for clients who might have left. These actions will provide valuable insights into how your clients perceive the new focus on client success and retention.

Subsequently, we will convene with the Partner Success Team to review our findings. The team will compare the capabilities of those trained with customer perceptions and retention rates. Additionally, they will review the compliance of the trained individuals by examining the client retention platform.

These various assessment points will enable the Partner Success Team to chart a clear path forward and subsequently transition to the Create phase to ensure the strategy is on target. Following this, adjustments will be made in the Execute phase to maximize the impact of the Clients for Life® client retention process.

Industries

This service is primarily available to the following industry sectors:

Healthcare

History

The healthcare business has undergone significant transformation, shaped by advancements in pharmaceuticals, biotechnology, technological innovation, regulatory changes, and evolving patient expectations. These factors have contributed to a more patient-centered, efficient, and accessible healthcare system, while also spurring substantial growth in specific sectors like pharmaceuticals and biotechnology.

One of the most transformative aspects of healthcare over the past ten years has been the rise of digital health technologies, such as electronic health records (EHRs) and telemedicine. EHRs have revolutionized how patient data is managed, improving communication between healthcare providers, enhancing patient safety, and streamlining administrative processes. Telemedicine, which gained rapid adoption during the COVID-19 pandemic, has expanded healthcare access, especially in underserved areas, and has reduced the barriers of distance and time in healthcare delivery. The convenience and efficiency of telemedicine are likely to sustain its relevance even as in-person healthcare services return to pre-pandemic levels.

The pharmaceutical industry has also seen tremendous growth and innovation over the last decade, with the development of new drugs, vaccines, and therapies. The industry’s rapid response to the COVID-19 pandemic, notably with the development of mRNA vaccines, underscored the potential of cutting-edge pharmaceutical research. The rise of precision medicine has enabled the creation of targeted therapies for specific conditions, such as cancer and rare genetic disorders. Advances in drug discovery, facilitated by artificial intelligence and machine learning, have shortened the timeline for new treatments, making the pharmaceutical industry more agile in responding to emerging health challenges.

The past decade has also seen increased regulatory reform aimed at improving healthcare access, reducing costs, and ensuring high-quality care. In the United States, the Affordable Care Act (ACA) continued to shape healthcare delivery, focusing on expanding coverage and promoting value-based care, where healthcare providers are incentivized to deliver quality care rather than a high volume of services. This approach has shifted the focus toward patient outcomes, driving efficiency and better overall healthcare performance.

In summary, the healthcare business over the past ten years has been marked by significant advances in pharmaceuticals, biotechnology, and digital health, alongside regulatory reforms. These changes have enhanced healthcare access, improved patient outcomes, and laid the groundwork for a more personalized and efficient healthcare system poised for future growth.

Current Position

Healthcare spending accounts for over 17% of the United States’ gross domestic product. It has evolved into a complex industry encompassing Medical Centers, Surgery Centers, Pharmaceuticals, Nursing Homes, Insurance Companies, Group Purchasing Organizations, and Institutions of Higher Learning. This is a multidimensional, multilayered industry that is highly interwoven and interconnected.

What was unheard of just 50 years ago has become commonplace today. Every year, new discoveries are made that not only increase our life expectancy but also enhance the quality of our lives. We now demand the best in health outcomes, a testament to the remarkable work of the pioneers of the not-too-distant past.

The challenge lies in providing the high level of care that is expected, at a cost that is reasonable for all, while ensuring it can be administered globally and remains focused on the patient’s mental, physical, and emotional well-being. This is no easy task. To meet this challenge, an ever-growing industry has developed to ensure that the quality of care we have come to expect is consistently delivered.

Government agencies, universities, medical associations, patient advocacy groups, insurance providers, and corporations have all attempted to define what healthcare should be today. With significant advancements in healthcare, a new level of oversight has emerged to ensure equitable, efficient, effective, and cost-conscious delivery of care.

However, when one lever in the delivery of care is adjusted, it affects all the others. This dynamic results in an ever-changing ecosystem of payers and providers who must collaborate to create the best possible healthcare system.

Future Outlook

There are no signs that the innovation we’ve seen in healthcare will slow down anytime soon. Our population continues to grow, advancements in medical research is reaching new heights, artificial intelligence is now becoming an integral part, and biotechnology is reaching new frontiers. All these developments will drive new demands and intensify competition in this sector. Unlike in the past, no single institution will dictate care.

Today, companies must be prepared to face high levels of competition from all sides. There is no longer a protected sector within the healthcare industry. Leading institutions like Merck, Mayo Clinic, and Blue Cross Blue Shield must work diligently to protect their market share moving forward.

This is a fast-paced industry where innovation and change occur daily, leading to an increasingly crowded marketplace. Providers are being redefined every day by public perception.

The healthcare consumer has become highly adept and aware of all the alternatives available. No longer a passive user of healthcare services, the modern consumer is an active and knowledgeable decision-maker who evaluates outcomes, levels of care, cost, and even the brand of providers.

In the past, businesses serving these institutions could rely on consistent revenue. Not anymore. In this new competitive environment, expectations are constantly evolving, and new competitors are entering the fray to meet the ever-changing demands of patients.

To survive, it is essential to have a strategy focused on retaining and growing with clients well into the future. There are no signs that the healthcare industry will stabilize; if anything, more disruption lies ahead.

Biotech

History

Biotechnology has experienced significant advancements and growth, revolutionizing various sectors of healthcare and life sciences. One of the most transformative areas has been gene therapy, which aims to treat or prevent diseases by modifying genetic material. Breakthroughs in this field have led to promising treatments for genetic disorders like spinal muscular atrophy and inherited retinal diseases, offering new hope for previously untreatable conditions.

Another major development has been the rise of immunotherapy, particularly in cancer treatment. Biotech innovations have enabled therapies like CAR-T (Chimeric Antigen Receptor T-cell) therapy, which engineers a patient’s immune cells to target and destroy cancer cells. This personalized approach has shown remarkable success in treating certain blood cancers and continues to expand into other cancer types.

The COVID-19 pandemic also demonstrated biotechnology’s critical role in global healthcare. The rapid development of mRNA vaccines by companies like Pfizer-BioNTech and Moderna showcased the potential of biotech innovation to address urgent public health crises. These vaccines, based on decades of research, were pivotal in curbing the pandemic and marked a turning point for mRNA technology, which is now being explored for other applications, such as flu and cancer vaccines.

Additionally, advances in CRISPR gene-editing technology have opened new frontiers in genetic engineering, allowing precise alterations to DNA. This breakthrough has potential applications ranging from treating genetic disorders to enhancing agricultural practices.

Overall, the last ten years have cemented biotechnology’s role as a driving force behind modern medical and scientific progress.

Current Position

The rapid growth of the biotechnology industry in recent years would have been unimaginable just a short time ago. Today, the industry generates over $215 billion in revenue and employs more than 319,000 highly skilled professionals. Investment in biotechnology has surged, with over 150 biotech companies going public in 2021 alone.

Between 2001 and 2020, biotech patents accounted for 5% of all patents filed globally. The United States leads the way, contributing 39% of these patents. The spark ignited in the late 20th century has now become a booming industry in the 21st century. However, the United States does not hold sole leadership. It controls 38% of the global market, followed closely by Europe with 28% and the Asia-Pacific region with 24%.

The recent pandemic showcased the biotech industry’s capabilities, as it played a crucial role in developing a vaccine that became a major turning point in the fight against COVID-19. When the world needed a solution, biotech was there to answer the call.

Biotechnology is now firmly established as a cornerstone of the larger pharmaceutical industry, having spurred the creation of its own ecosystem. This includes the Specialty Pharmacy sector, which was born to ensure the quality and care of administering these complex compounds. Additionally, niche insurance, payer systems, and logistics companies have emerged to ensure that patients have access to these vital drugs.

Despite its success, there is still much work to be done, and the industry remains characterized by a high level of risk versus reward. Much of the underlying science and technology is still under development, and research and development costs can be steep with no guarantee of return on investment. Nevertheless, investors continue to be drawn to this highly promising industry.

Future Outlook

The biotechnology industry shows no signs of slowing down. In fact, projections suggest that the industry could more than triple in size by 2033, reaching over $763 billion. This growth will be driven by significant contributions from the United States and Europe, alongside the rapid development of markets in China, India, and Japan. As clinical development, government initiatives, standardized regulatory pathways, clinical trials, expedited product approvals, and enhanced reimbursement policies take shape, the industry is poised for accelerated global expansion.

What began as a sector focused primarily on medications has now diversified. Biotechnology now spans genetics, agriculture, and medical applications. When you consider that we’ve unlocked the secrets of DNA—the fundamental building block of life—the possibilities seem endless. Look for new applications such as bio-information and bio-services to expand in the coming years.

To sustain this growth, increased investment is essential. The biotech industry has become highly competitive, both among companies and across regions. This competition has led to a surge in collaborations, mergers, and acquisitions as the race to market intensifies. Biotech companies are increasingly seeking synergies, efficiencies, and market presence to stay ahead in this ever evolving and expanding market.

No longer can a biotech company rely on being one of the few with a new breakthrough that will remain unchallenged for years. Companies must focus not only on growth but also on retaining their market share, while those providing services to this rapidly expanding industry must do the same or they will be lost in the past.

Logistics

History

The logistics industry is a tale of evolving efficiency and innovation, reflecting broader economic and technological advancements. It begins in ancient civilizations where the logistics of moving goods was primarily a matter of necessity. Over the past decade, the logistics industry has seen substantial growth, driven by technological advancements, global trade expansion, and the rise of e-commerce. Logistics, which involves the management of the flow of goods from origin to destination, has become a cornerstone of modern supply chains, transforming in response to shifting consumer behaviors and market demands.

The explosive growth of e-commerce, led by companies like Amazon, Alibaba, and other online retailers, has been a major driver of the logistics market. As consumer demand for fast, reliable delivery increased, logistics companies had to adapt by investing in last-mile delivery solutions, warehousing automation, and real-time tracking technologies. The rise of same-day and next-day delivery services created new opportunities for companies to differentiate themselves by improving speed and efficiency.

Technological innovation has played a significant role in shaping logistics over the past ten years. Automation, artificial intelligence (AI), and data analytics have streamlined operations, allowing companies to optimize routes, improve inventory management, and forecast demand more accurately. Warehouse automation, through the use of robots and AI-driven systems, has dramatically increased efficiency and reduced operational costs. Meanwhile, AI-powered logistics platforms have helped companies improve decision-making by offering real-time insights into supply chain performance.

The global supply chain disruptions caused by the COVID-19 pandemic highlighted the importance of a resilient logistics infrastructure. Companies were forced to rethink their strategies, often turning to digitalization and flexible supply chain models to mitigate the impact of lockdowns and transport restrictions.

Overall, the logistics industry has experienced remarkable growth over the past decade, evolving into a highly sophisticated and technology-driven sector. This transformation is expected to continue, with further innovations such as autonomous vehicles, drones, and blockchain technology set to revolutionize the logistics landscape in the coming years.

Current Position

The logistics industry is a blend of rapid technological advancements, shifting consumer expectations, and complex global challenges. This sector is undergoing significant transformation driven by several factors.

First, technological stands at the forefront of the revolution. The integration of technologies such as artificial intelligence (AI), machine learning, and the Programable Object Interfaces (POI) is revolutionizing logistics operations. AI and machine learning are enhancing predictive analytics, improving demand forecasting, and optimizing routes. POI devices provide real-time tracking and monitoring of shipments, offering greater visibility and control throughout the supply chain. Automation, including the use of autonomous vehicles and drones, is also gaining traction, promising to streamline warehousing and delivery processes.

E-commerce has dramatically reshaped the logistics landscape. The surge in online shopping has created a demand for faster, more flexible delivery options. This shift has led to an increase in last-mile delivery services, where logistics companies are focusing on optimizing delivery times and enhancing customer experiences. The growth of e-commerce has also accelerated the adoption of technologies like robotics and automated sorting systems in warehouses to manage the high volume of orders efficiently.

Global disruptions, such as the COVID-19 pandemic and global conflicts, have highlighted the vulnerabilities in supply chains and underscored the need for greater resilience and flexibility. Companies are reevaluating their supply chain strategies, diversifying sources, and investing in technology to build more robust and adaptive logistics networks.

The logistics industry today is marked by technological innovation, evolving consumer demands, and a focus on sustainability and resilience. The sector is navigating a complex landscape, balancing efficiency with the environmental and global disruptions and adapting to the ever-changing global market.

Future Outlook

The future of the logistics industry will be shaped by advancements in technology, evolving consumer expectations, and an increasing emphasis on sustainability. As the sector continues to adapt, several key trends are anticipated to drive its transformation.

Technology will remain a pivotal force in the logistics industry. Innovations such as artificial intelligence (AI), machine learning, and the Programable Object Interface (POI) will further enhance supply chain efficiency. AI will enable more accurate demand forecasting and predictive maintenance, while POI devices will continue to provide real-time tracking and visibility. Automation, including autonomous vehicles and drones, will revolutionize transportation and warehousing, leading to faster and more cost-effective delivery solutions.

E-commerce will continue to influence logistics significantly. The growing expectation for rapid, flexible delivery will drive further advancements in last-mile delivery solutions. Companies will invest in advanced robotics, automated sorting systems, and micro-fulfillment centers to meet the demand for quick and efficient service. Additionally, the rise of omnichannel retailing will require seamless integration of online and offline logistics operations.

Sustainability will also become a central focus. The logistics industry will increasingly prioritize reducing its environmental impact by adopting green technologies. Electric and hydrogen-powered vehicles, optimized route planning to reduce fuel consumption, and sustainable packaging solutions will become standard. Companies will also enhance efforts to minimize waste and carbon emissions across their supply chains.

The need for resilience and adaptability will be underscored by global disruptions, such as pandemics and geopolitical tensions. Future logistics networks will be designed to be more flexible and robust, incorporating risk management strategies and diversified supply chains.

Overall, the future of logistics will be defined by technological innovation, a commitment to sustainability, and the ability to adapt to a dynamic global environment. These factors will drive the industry towards greater efficiency, responsiveness, and environmental stewardship. Those who meet the expectation of their clients and align resources accordingly will succeed.

Advertising

History

The past decade has been profoundly shaped by the rise of social media and technological innovations. This era has seen a major shift from traditional media outlets, such as television, radio, and print, to digital platforms, where social media giants like Facebook, Instagram, Twitter, and TikTok have become dominant forces in the advertising landscape. The explosion of these platforms has allowed advertisers to reach highly targeted audiences in ways that were previously impossible.

One of the most significant changes in advertising during the social media era is the ability to use data-driven strategies to personalize ads. Platforms like Facebook and Google collect massive amounts of user data, allowing advertisers to target ads based on demographics, interests, behaviors, and even location. This precision has led to more effective campaigns, with advertisers able to track engagement, conversion rates, and return on investment (ROI) in real-time.

Influencer marketing has also grown exponentially over the last decade. As social media became more integrated into people’s lives, influencers — individuals with large, engaged followings — emerged as key partners for brands. By leveraging influencers, brands have been able to reach audiences in a more authentic, relatable manner, as consumers often trust recommendations from influencers more than traditional advertisements.

In addition to social media, technological innovations such as artificial intelligence (AI) and machine learning have revolutionized advertising. AI-powered tools allow for the creation of programmatic advertising, where automated systems purchase ad space in real-time, optimizing campaigns for performance. Machine learning algorithms have also enabled dynamic content creation, with ads being personalized based on user interactions and preferences.

Another key trend has been the rise of video content, with platforms like YouTube, Instagram Reels, and TikTok leading the charge. Video ads have become highly engaging, driving higher levels of user interaction and brand recall compared to static ads. Additionally, brands have adopted storytelling techniques, creating immersive ad experiences that resonate emotionally with audiences.

The COVID-19 pandemic further accelerated the shift toward digital advertising, as businesses were forced to adapt to a more online-centered world. E-commerce and social commerce grew rapidly, and advertisers sought new ways to engage consumers confined to their homes.

Looking forward, innovations such as augmented reality (AR), virtual reality (VR), and the metaverse are set to shape the next wave of advertising. AR filters and VR experiences allow users to interact with brands in new, immersive ways, while the development of the metaverse offers entirely new digital environments for brand engagement.

In summary, the past decade has seen advertising transform into a data-driven, personalized, and highly interactive domain, largely driven by social media and emerging technologies. As digital platforms continue to evolve, the future of advertising will likely be defined by even more immersive and targeted approaches.

Current Position

The advertising industry today is a dynamic and rapidly evolving landscape shaped by technological advancements, shifting consumer behaviors, and heightened scrutiny around data privacy.

One of the most significant trends is the growing dominance of digital and social media platforms. Advertisers are increasingly allocating budgets to digital channels, driven by their ability to offer precise targeting and real-time analytics. Platforms like Google, Facebook, and TikTok have become essential for reaching audiences, leveraging algorithms and user data to optimize ad performance and engagement.

However, this digital shift comes with challenges. Privacy concerns have led to stricter regulations, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA). These regulations are reshaping how data is collected and used, pushing advertisers to adopt more transparent and ethical practices. The rise of privacy-centric technologies, like Apple’s App Tracking Transparency, has further complicated targeting strategies, forcing the industry to innovate and adapt. So companies are listening to the customer and are not sharing certain information and added restrictions.

Moreover, the advertising landscape is increasingly characterized by a demand for authenticity and inclusivity. Consumers are becoming more conscious of social issues and expect brands to reflect their values. This has led to a rise in purpose-driven marketing, where brands are expected to engage in social and environmental causes genuinely rather than superficially. This has added an extra risk as advertisers try to project values without overtly offending.

The industry is also witnessing a surge in creative formats, such as interactive and immersive ads driven by augmented reality (AR) and virtual reality (VR). These technologies offer new ways for brands to engage with consumers, creating more memorable and engaging experiences.

Overall, the advertising industry is in a state of flux, balancing innovation with regulatory challenges and shifting consumer expectations. Brands that can navigate these changes while maintaining authenticity and leveraging new technologies will be well-positioned for success in this evolving landscape.

Future Outlook

The future of advertising promises to be an exhilarating blend of advanced technology, deeper personalization, and ethical responsibility. As we move beyond today’s trends, several key developments are expected to shape the industry.

Firstly, the integration of artificial intelligence (AI) and machine learning will revolutionize advertising strategies. AI will enhance the ability to predict consumer behavior with unprecedented accuracy, allowing for hyper-personalized ad experiences. Predictive analytics and automated content generation will become more sophisticated, creating ads that are not only targeted but also contextually relevant and engaging.

Augmented reality (AR) and virtual reality (VR) will likely play a significant role in shaping the future of advertising. These immersive technologies will offer consumers interactive experiences that go beyond traditional formats. For instance, AR could allow users to virtually try on products before purchasing, while VR could create fully immersive brand experiences.

Trust will continue to be an area of focus. In response, the industry will need to prioritize transparency, data protection, and ethical practices. Brands that build trust through responsible data use and clear communication will stand out.

Sustainability and social responsibility will become even more central to advertising strategies. Consumers will increasingly favor brands that actively contribute to social and environmental causes. This shift will drive brands to not only communicate their values but also demonstrate genuine commitment to positive impact.

Finally, the rise of decentralized platforms and blockchain technology could transform how ads are distributed and how transactions are verified, offering greater security and transparency.

In summary, the future of advertising will be defined by advanced technology, personalized experiences, ethical practices, and a commitment to social responsibility. Brands that can adapt to these evolving dynamics will be well-positioned to thrive in the next era of advertising. We have come far from the first printing press!

Insurance

History

From 2015 to today, the insurance industry has experienced rapid transformation, driven by advancements in technology, shifting customer expectations, and emerging global risks. This period has seen the rise of insurtech, new regulatory frameworks, and the growing importance of data analytics and personalized products.

The mid-2010s marked the beginning of the insurtech boom, with startups and established companies harnessing technology to disrupt traditional insurance models. Insurtech companies, like Lemonade and Root, leveraged artificial intelligence (AI), machine learning, and mobile technology to simplify the process of buying and managing insurance policies. These firms offered more efficient, customer-centric services, challenging traditional insurers to innovate and improve their digital capabilities. AI and chatbots enabled faster claims processing, while mobile apps allowed users to manage policies and file claims easily.

During this period, data analytics became central to the insurance industry. Insurers increasingly relied on big data, AI, and telematics to assess risk more accurately and tailor products to individual customers. In auto insurance, usage-based policies using telematics devices became popular, allowing premiums to be based on driving behavior rather than traditional risk factors. Similarly, health and life insurers adopted wearable technology to monitor policyholders’ health, offering incentives for maintaining healthy lifestyles.

The insurance industry also faced new regulatory challenges. The introduction of stricter data privacy regulations, such as Europe’s General Data Protection Regulation (GDPR) in 2018, forced insurers to adopt robust cybersecurity measures and improve data handling practices. Additionally, emerging risks like climate change and the increasing frequency of natural disasters led insurers to develop new catastrophe models and products to protect businesses and individuals from escalating environmental threats.

Since 2015, the insurance industry has evolved significantly, with digital transformation, data-driven personalization, and an increasing focus on new global risks shaping its trajectory. These changes have pushed insurers to innovate, improve customer experiences, and create more flexible and adaptive products.

Current Position

Today, the insurance industry continues to be as vast and complex as the world around it. On the surface, the industry is perceived as a slow growing, safe sector for investors. It does perform solidly in the face of the ups and downs of the economy, and the stability of the industry is very strong. However, each sector has its own market and volatility.

There are three main sectors to focus on when looking at this industry: Property/Casualty, Life and Annuity, and Health Insurance. Property/Casualty has shown a relatively stable increase over the past ten years. Life and Annuity has varied over the same time, with growth one year followed by declines the next.

Health Insurance is a distinct sector and can be further broken down into medical coverage, pharmacy coverage, and long-term care insurance. In total, 92% of people in the United States have health insurance today. Health Insurance can be divided into Employment-based, Medicaid, Medicare, and direct purchase. The majority of those insured are covered by employment-based coverage at over 54%, followed by Medicaid and Medicare each at 19%, and direct purchase at 10%.

The insurance industry is not immune to competition. New rivals are showing up daily in what once had strong barriers to entry. Technology and innovation have made way for everything from major technology firms to small shops. Existing insurance firms must shift from product to service to hold off the competition. This means insurance companies need to focus on the customer experience. Today’s environment begs insurance companies to look forward.

Future Outlook

Since 2015, the insurance industry has faced increased competition, changing customer expectations, greater technological advancements, and the impact of climate change, among other challenges. As a result, profits have been under pressure, leading to a rise in premiums on average to offset the losses.

The insurance model is adapting to address profitability concerns and the evolving needs of clients. The traditional product-centric models based solely on price are no longer effective. Insurance companies are exploring new distribution and service channels, emphasizing speed, and offering solutions online, such as quotes and coverage.

The era of one-size-fits-all insurance offerings is fading, with a shift towards competitive quotes and personalized offerings. AI and automation are expected to play a significant role in the industry’s future, focusing on high-touch, customer-centric, and efficient results.

A notable example of industry change can be seen in pharmaceutical insurance. Social and political pressures are prompting Pharmacy Benefit Managers (PBMs) to reconsider their rebates and practices. While PBMs are adapting, the question remains whether they can adjust quickly enough or if new, more customer-centric entrants will capture market share swiftly. These new entries are listing to the customer and offering a flat fee rate which is appealing to many in the market.

Overall, the insurance industry is entering a new era. Third-party distributors have gained a stronger presence and are particularly focused on servicing their client base. This shift means greater efforts are necessary to retain not only individual consumers but also the third-party distributors wielding significant negotiating power on behalf of their clients.

Locations

This service is primarily available within the following locations:

Atlanta

History

Over the last decade, Atlanta has solidified its reputation as a hub of business innovation and growth. As one of the fastest-growing metropolitan areas in the United States, it has attracted major corporations and startups alike. Atlanta’s rise as a business powerhouse can be attributed to several factors, including its strategic location, robust infrastructure, and diverse talent pool. The city is home to several Fortune 500 companies, such as Coca-Cola, Delta Airlines, and Home Depot, which have expanded their operations, contributing significantly to the local economy.

The technology sector, in particular, has flourished in Atlanta, earning it the nickname “Silicon Peach.” Tech giants like Microsoft and Google have established major operations in the city, while a thriving startup ecosystem has emerged, supported by accelerators like Techstars and Atlanta Tech Village. The fintech industry, driven by companies like NCR and Global Payments, has also played a pivotal role in Atlanta’s economic evolution.

Atlanta’s business landscape has also been shaped by its commitment to diversity and inclusion. The city has become a leader in promoting minority-owned businesses, especially in tech and real estate, fostering a more inclusive economy. Its extensive transportation networks, including the world’s busiest airport, Hartsfield-Jackson, and well-developed highways, have further bolstered Atlanta’s appeal to businesses seeking connectivity and efficiency.

Over the last ten years, the city has positioned itself as a dynamic business center with a bright future, offering ample opportunities for both entrepreneurs and established companies to thrive.

Current Position

Atlanta has also become a hub for education and culture, with numerous universities and colleges in the area and a thriving arts and music scene. The city is home to the High Museum of Art, the Atlanta Symphony Orchestra, and the Alliance Theatre, among many other cultural institutions. Atlanta has truly grown from its humble beginnings.

In recent years, Atlanta has also become a major player in the film and television industry, earning the nickname “Hollywood of the South.” The city has attracted numerous film and television productions, thanks to its diverse locations, skilled workforce, and generous tax incentives.

However, Atlanta is more than the glitz and glamour of the Hollywood of the South. Atlanta boasts 16 of the Fortune 500 companies. Besides the film and television industry Atlanta is home to strong aviation contributing 34.8 billion in revenue, financial technology contributing 72 billion and health care and biotechnology sectors. The healthcare and biotechnology sector is ranked 10th for overall life science jobs. With such notable institutions as the Centers for Disease Control, Emory University, and a host of biotech companies.